14/4/26

What I Spent This Week as a Project Lead Making £43k

Ever wondered how others really manage their money?

Ever wondered how others really manage their money?

In the A Week in My Wallet series, we share it all, because talking about money shouldn't be off-limits.

Every week, an anonymous member shares a week of their spending: no names, no filters, just honest stories about life's everyday financial choices.

Ready to join the conversation and help make money talk less taboo? Share your own story via our form here.

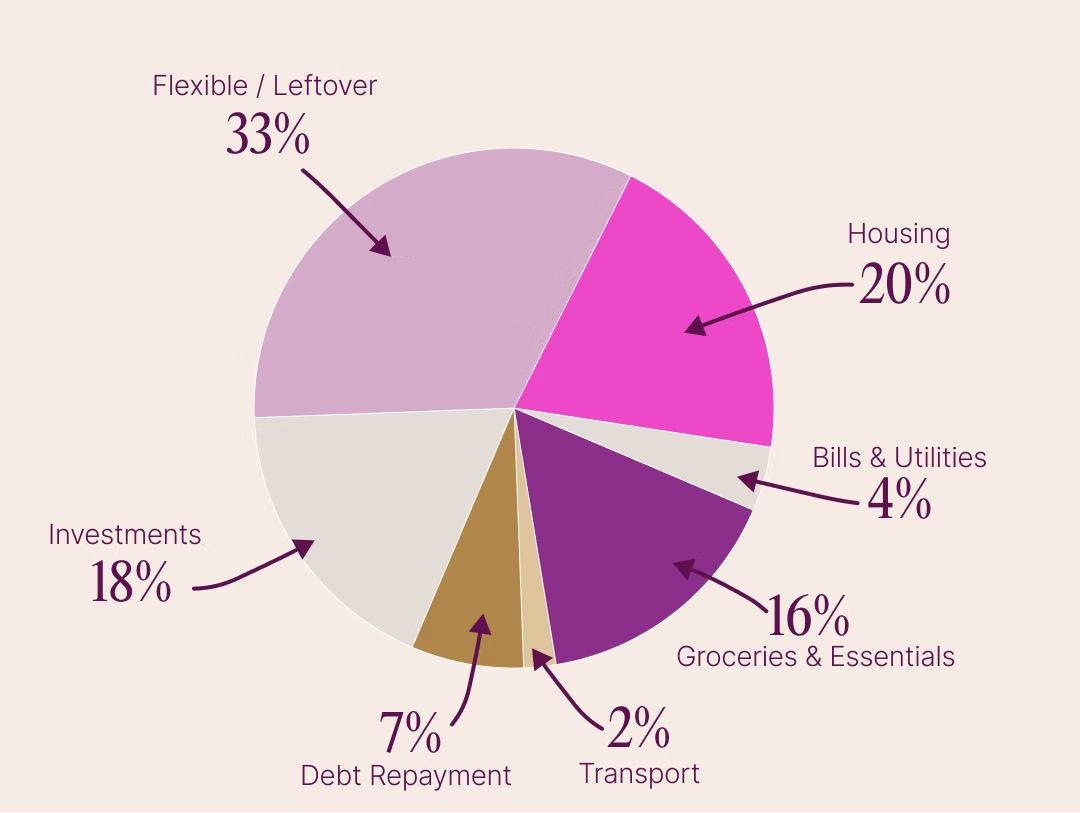

Monthly Take-Home Pay (after tax): £2,745

Do you share expenses with someone? Yes, a partner

What is your overall monthly budget?

- Rent includes council tax: £544

- Bills, Subscriptions & Utilities: £114

- Monthly debt for eye surgery: £191

- Transport: £50 for Uber rides or occasional train rides (as I work from home, no car, mostly walk to places)

- Groceries & Essentials: £429 (including 1 cat expense, and a monthly charity donation to sponsor a Cambodian girl to continue her education which to me is an essential, it may be different to other people)

- Investment Contributions: monthly £500 set but I do invest more sometimes in addition to the £500 set.

Amount left each month after essentials (to spend, save or invest): £914

Dependents (if any): 1 cat

My Relationship with Money

Growing up, did your parents or guardians educate you around money?

I grew up in Cambodia, raised by my single mom and my grandparents. My dad never supported us financially, so my grandma became the person who shaped how I think about money, she was like a mom, a dad and a grandma.

She had been through war, revolution, genocide, and even lived as a refugee in Vietnam before returning to Cambodia so she understood the value of every grain of rice, literally. She was strict, sometimes unreasonably so, but she taught me principles, discipline, and humility from a very young age. She ran multiple small family businesses with my mom, a café, a restaurant, a convenience store, even a traditional spa, and she eventually retired in her 50s after realising the businesses weren’t profitable anymore.

She lived modestly but managed to support all of us, including paying for our education (even public school/university isn’t free in Cambodia) and other expenses. She never spoiled us. No allowances, no unnecessary spending. If I wanted something even as a 6 years old until young adult, I had to “pitch” why it mattered and what value it brought. That shaped my entire relationship with money.

What was your first job and why did you get it?

I started trying to make money when I was about 10. Asking my grandma for anything was tough, so I found my own ways like being a middle person between my classmates and a fish shop I visited after school, or buying things for classmates and taking a small commission.

My first official job was as a part-time receptionist at a physiotherapy clinic when I started my first year of uni at 16. I wanted independence, and I didn’t want to rely on my grandma. From there, I kept finding small ways to earn, ordering desks and chairs from China, assembling them myself, and selling them on Facebook; doing volunteer work that led me into the startup world; switching part-time jobs to learn more skills and earn a bit more.

By the time I finished my undergrad, I already had a full-time job lined up at one of the big banks in Cambodia.

Did you worry about money growing up?

Yes, absolutely. Growing up in a developing country without free healthcare or financial safety nets means you’re always aware of how fragile everything is. My grandma taught us to prepare for the worst, and while that mindset kept us safe, it also made me an overthinker.

Even as a kid, I worried about money because I saw how hard my mom and grandma worked just to cover essentials, there was no budget for holidays or eat out once a week or once a month or a year.

At what age did you become financially responsible for yourself and do you have a financial safety net?

I became financially responsible for myself around 21. By then, I had multiple income streams and a full-time job in Cambodia. That was the first time I felt truly independent.

As for a safety net, I wouldn’t say I have a big one. I’ve always saved and planned because I grew up knowing that if something goes wrong, there isn’t a government system to catch you. Now that I live in the UK, things are different, but that mindset is still in me as I'm not a citizen/PR to be eligible for any government safety net. And with my grandma getting older and dealing with her health issues, plus other family responsibilities, I still feel the pressure to be financially prepared.

Do you worry about money now?

Yes, I do. It’s ingrained in me. I’m not extremely frugal, I still save enough to travel to Asia once or twice a year but I think very carefully before making big purchases. Sometimes I’ll wait one or two years before buying something, even if I can afford it. For example, my eye laser surgery, it took me almost 3 years to actually doing it. Part of that comes from watching my grandma save her whole life but never really spend on enjoyment, no holidays, no days out, no treats to herself or family members.

Essentials always came first, preparation for the worst future came second. I understand why, but I’m trying to find a healthier balance for myself. Still, with the current economy, family responsibilities, and my grandma’s health, I probably worry about money more than ever.

What is your biggest money regret?

I don’t think I have a major money regret. I’ve made some mistakes like getting tricked by a startup partner and losing money but I see those as expensive lessons rather than regrets. If anything, I sometimes think about how different my financial journey might have been if I’d grown up in a country with systems like ISAs, anyone above 18 years old can start to invest in stocks/shares, free education, or easy access to other types of investing/earning. But I also recognise that being where I am now with my background is also a privilege, and I don’t take that for granted.

What financial goals are you working towards?

Compared to others in the UK, I’m probably around the average-income range, but I don’t really compare myself to people who earn more or less. My focus is on improving my own situation, building a comfortable life with my wife here in the UK, and supporting my family back home in Cambodia (when they need it in the future).

I take money seriously, but health, happiness, and family time come first. My long-term financial goal is to not rely solely on my full-time UK job. I’d love to have multiple income streams and more freedom, but because of my current visa, I’m limited in what I can do. Hopefully by the end of this year, my visa situation will change and I’ll finally feel less tied to just one job.

A big goal for me is to be able to travel back to Cambodia or on a holiday somewhere whenever I need to without stressing about the cost so I can see my family more often and travel more with my wife. And since my wife is British, the UK is home too. I just want us to live comfortably together, without feeling restricted or stretched.

Who is your financial role model (if any), and why?

My biggest financial role model is my grandma. She shaped almost everything about how I think about money. She wasn’t formally educated in finance, never went to university, but she had incredible instincts, she built her own fortune through small family businesses, retired in her 50s, and still managed to support all of us. And she did all of that after surviving some of the hardest things a person can go through: civil war, revolution, genocide, being a refugee, and starting over again in Cambodia.

What inspires me most is how disciplined and grounded she was. She taught us not to waste anything, to understand the value of money and food, and to stay humble no matter what. She never spoiled us, but she always made sure we had what we needed. Even though she could be strict, her lessons stuck with me especially the idea that money should bring value.

I think the way I save, the way I plan for the worst, and even the way I hesitate before making big purchases all come from her. However, I am different in a way that I believe money should also for comfort and enjoyment. She’s the reason I became financially independent so young, and the reason I still take money seriously today.

Reflections on My Spending Habits:

Looking back over the week, my everyday spending was actually quite controlled, with most costs going toward essentials like groceries, transport, and routine plans. The biggest jumps came from planned one-off expenses, such as the supplements which is 3 month worth and the holiday resort booking, which skew the total but don’t reflect my usual habits. Overall, I’m consistent and intentional with day-to-day spending.

What I Spent in a Week

Day 1: Monday - £42.90

Boots: £41.00 3 month supplements

Tesco: £1.90

Day 2: Tuesday - £23.97

Takeaway £14.37

Uber ride £4.70 (to train station for MCR office visit)

Uber ride £4.90 (train station to home)

Day 3: Wednesday - £16.99

Pet health monthly plan - £16.99

Day 4: Thursday - £10.09

Tesco: £10.09

Day 5: Friday - £0

Nothing to spend as working from home and foods at home.

Day 6: Saturday - £44.54

Lidl: £36.66

Amazon Ipad case: £7.88

Day 7: Sunday - £233.22

SIM card plan: £8.24

Booked resort stay during Apr holiday with wife: £224.98

Total Weekly Spend: £371.71