29/4/26

What I Spent This Week as a Programme Manager Making $111K

Ever wondered how others really manage their money?

Ever wondered how others really manage their money?

In the A Week in My Wallet series, we share it all, because talking about money shouldn't be off-limits.

Every week, an anonymous member shares a week of their spending: no names, no filters, just honest stories about life's everyday financial choices.

Ready to join the conversation and help make money talk less taboo? Share your own story via our form here.

Monthly Take-Home Pay (after tax): £4,388 ($5,880)

Do you share expenses with someone? My husband and I combine our salaries on pay day and then decide jointly each month where to allocate our funds. For ease of tracking 1 week I’ve divided everything as if it's 50/50.

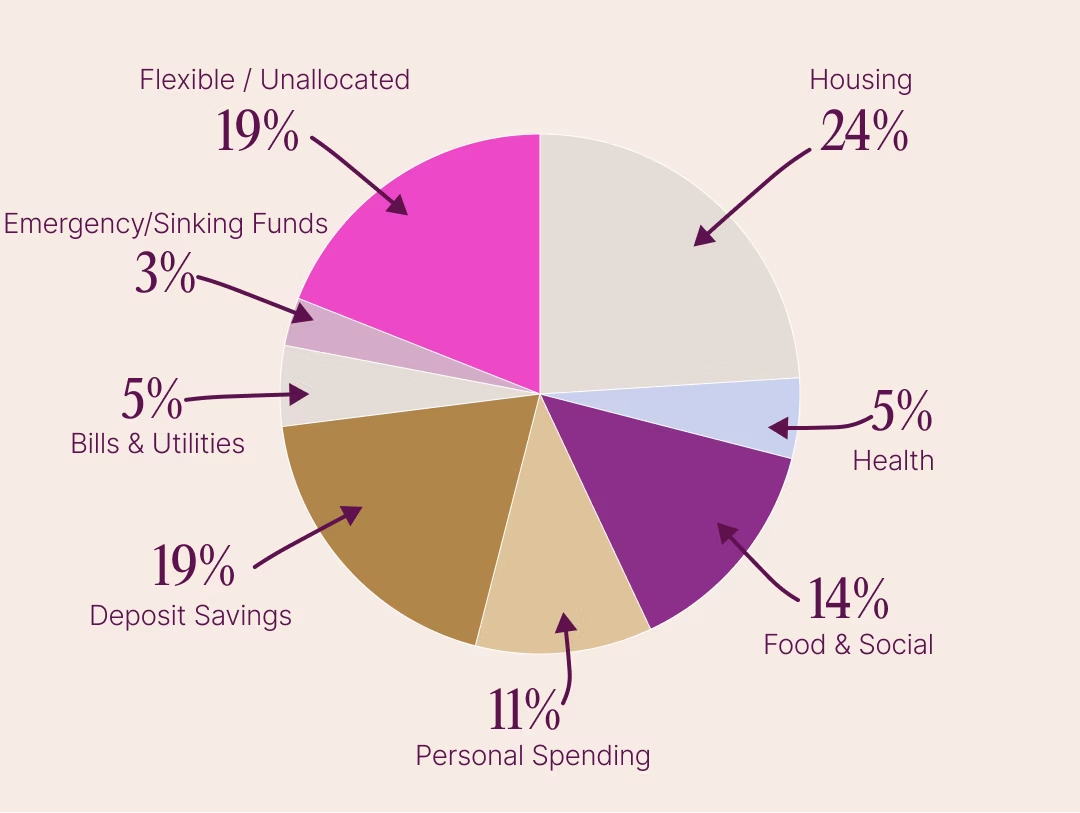

What is your overall monthly budget? £3,600 ($4,824)

- Rent £1050 ($1,407)

- Bills £225 ($302)

- Food and social £600 ($804)

- Own spending £500 ($670)

- Deposit £850 ($1,139)

- Health £225 ($302)

- Emergency fund £50 ($67)

- Big birthday £100 ($134)

Amount left each month after essentials (to spend, save or invest):

Zero because we do a zero-based budget, if I don’t spend my allocated ‘pocket money’ each month I either invest it or keep it accumulating for future months.

Dependents (if any): 0

My Relationship with Money

Growing up, did your parents or guardians educate you around money?

I can remember being taught to save up my pocket money if I wanted to a specific toy. So I learnt how to save up and be patient, but never about budgeting or how much things really cost.

What was your first job and why did you get it?

Working in a cafe at 18. I was very fortunate that my parents didn’t want me to work until finished school so I could focus on my studies. I got it because I wasn’t getting pocket money any more and everyone at uni had a part time job while studying.

Did you worry about money growing up?

Never. I was incredibly lucky to grow up well off and I genuinely didn’t understand when people complained about bills because to me there was always a bank account to withdraw from.

At what age did you become financially responsible for yourself and do you have a financial safety net?

Age of 21 when I moved out of home and across the country. I slept on a mattress on the floor because I couldn’t afford to buy a bed. Back then I had the safety net of Mum and Dad but I was also stubborn to make it by myself. Now I have emergency funds set up and my husband would support me if we needed.

Do you worry about money now?

Yes, I really worry about having enough money in retirement. Neither my husband or I had any pension until late 30s and massively trying to make up for it now. We had two back to back emergencies which used up all our emergency funds set and put us in debt, so now I’m always worried our emergency fund isn’t enough and that our pension will never be.

What is your biggest money regret?

Not putting money aside for pension or paying off student loans sooner. In my 20s, I really didn’t understand how much interest student loans was increasing by each year to understand the need to pay it off as a priority.

What financial goals are you working towards?

Saving up for a big birthday overseas trip for my Mum’s 60th, saving up for a deposit for a flat, boosting our emergency fund, and adding to our pension. We change each month where we focus our savings to maximise tax benefits. It’s hard to believe we’ll ever have enough for all goals, which is part of why we change how much we set aside for each every month.

Who is your financial role model (if any), and why?

My friends. I’m fortunate to have lots of friends in similar stage of life to share tips and tricks with keeping a budget and saving goals. We all inspire each other.

Reflections on My Spending Habits:

I feel extremely privileged to be able to afford quality of life and still maintain savings. I sometimes find it too easy to spend on convenience like Ubers and meal kits. I’m also so very grateful to WFH majority of the week as I save money on transport and coffee out.

What I Spent in a Week

Day 1: Monday - £90.45 ($121)

£12.95 ($17) — Groceries bits and pieces for the week

£77.5 ($104) — Council tax for the month

Day 2: Tuesday - £6.40 ($9)

£6.40 ($9) — Transport to office

Took leftovers for lunch to work

Day 3: Wednesday - £0 ($0)

No spend day, WFH, and weekly food prep for meals

Day 4: Thursday - £27.96 ($37)

£27.96 ($37) — Weekly meal kit

Day 5: Friday - £11.50 ($15)

£2.50 ($3) — Transport

£9 ($12) — Uber home from Eid

Day 6: Saturday - £2,050.50 ($2,748)

£13.50 ($18) — Coffee and cake with a friend, my treat

£2,015 ($2,700) — For permanent visa in UK

£22 ($29) — Groceries for the week and bits for the house

Day 7: Sunday - £0 ($0)

No spend day

Food prep at home and prepare for the week

Total Weekly Spend: £2,186.81 ($2,930)