24/12/25

Your Money Reset Part 4 - Build a Budget That Supports Your Life

Budgets sound boring - we get it. But a budget can actually be freeing. Here’s our ultimate guide, plus a free template to make it easy.

Before we talk about budgets, let’s pause and look at how far you’ve already come.

In Part One, you reviewed your financial year — where your money actually went, what worked, and what didn’t.

In Part Two, you explored your money story and defined your values — the deeper reasons behind your financial choices.

In Part Three, you envisioned your dream life and turned that vision into clear, prioritised goals.

All of that mattered.

Because now, you’re no longer guessing.

You know what matters to you. You know where you want to go.

That’s where budgeting comes in!

A budget is not a punishment

If budgeting has ever felt intimidating, rigid, or like something you “fail” at, you’re not alone.

The problem with most budgets (as we're sure you've experienced before) is they don't actually work!

But we're here to change all of that.

Packed with tips and tricks and our free budget planner, it's in this part of the money reset mini-series that you'll quickly realise that a budget is far from restricting.

Quite the opposite - it's empowering!

A budget is simply a plan for how your money supports your priorities.

It’s a way to decide — in advance — what you want your money to do for you.

When done right, a budget makes your life calmer.

When done right, a budget makes your life calmer

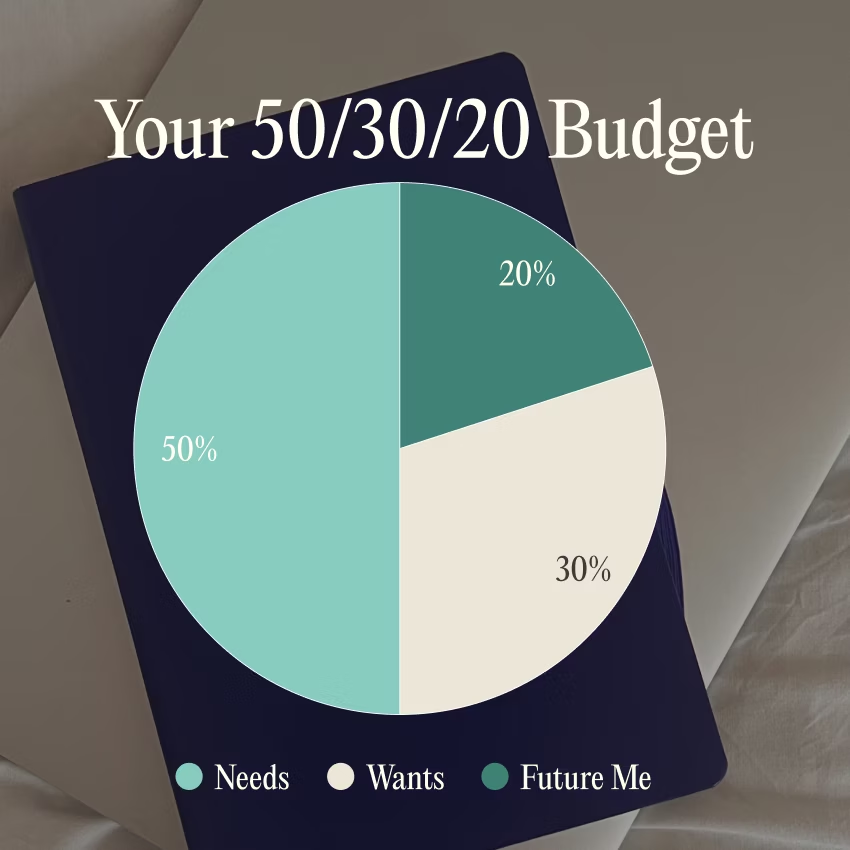

The 50/30/20 rule explained

There are so many different ways to budget, and no single method works for everyone.

But if there’s one framework we keep coming back to — and recommend again and again — it’s the 50/30/20 rule.

It’s simple, flexible, and designed for real life.

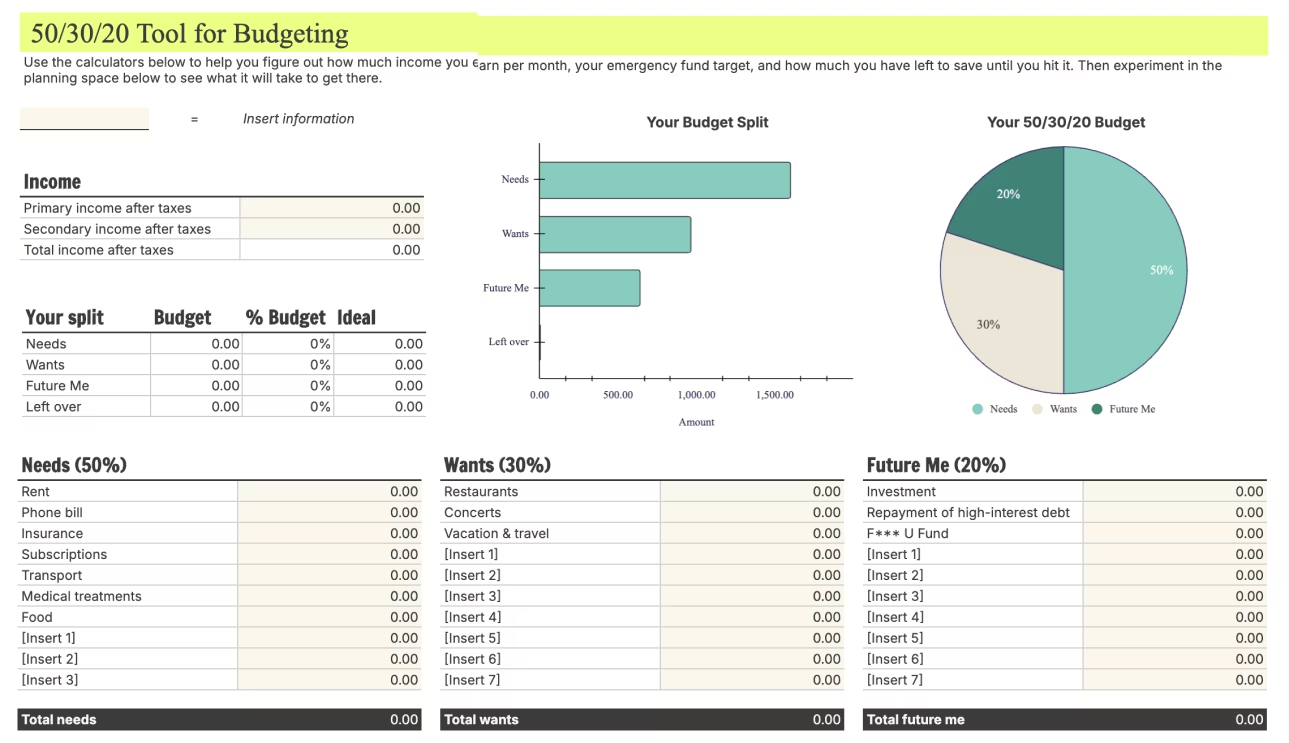

The 50/30/20 rule divides your income into three broad categories: needs, wants and future you. Let’s go through each..

50% - Needs

50% of your income should go towards necessities. This is things like bills, transportation, rent, insurance, food.

Basically, anything you have to pay for, even though you don't really want to.

30% - Wants

30% of your income goes towards fun. Because in life you need to have fun and spend your money doing what you love.

Why?

Well, even though you don't really need the takeaway sushi, the fancy wine, the weekend getaways, or the spa days, if you eliminate all the fun stuff and the things that bring you joy, you're definitely not going to stick to your budget.

20% - Future You

This is where your goals live. Emergency savings, investing, debt repayment, and anything that builds long-term security or freedom.

The 50/30/20 rule is simply a guideline and not a strict set of rules.

How we might categorise things will be different depending on who you are and the lifestyle that you have.

For example, some people might categorise going to the gym as a need while others as a want.

The figure will also depend on your income and, for example, your housing needs.

So you might end up with a case of 60% instead of the recommended 50%.

And that's okay.

The most important thing is to keep track of your costs, prioritise your expenses, and make sure that you're doing everything possible to save and invest for future you.

This 50/30/20 rule is a framework to be inspired by! But you can adjust it as your want.

How this connects to your goals

In Part Three, you didn’t just dream, you prioritised.

You sorted your goals into must-haves and nice-to-haves.

Now your budget helps you reflect those choices.

Let’s look at an example at how goals become budget decisions.

In Part Three, Anna identified her must-haves as:

- Building an emergency fund

- Paying down high-interest credit card debt

Her nice-to-haves were:

- A summer trip

- Investing more aggressively later

So inside her 600 “Future You” money, she decides:

- 400 goes toward emergency savings and debt repayment (must-haves)

- 200 goes toward investing and travel savings (nice-to-haves)

That’s what prioritisation looks like in practice. Not doing everything at once but doing the right things first.

Action: build your first aligned budget

We’ve created a free 50/30/20 budgeting template to help you turn everything you’ve worked on so far into a clear, practical plan - without overthinking it.

Make the framework work for you

A good budget works in real life not just on paper.

Life happens. Circumstances change.

We pivot our careers, get pay rises and so on.

When these shake ups arise (as they inevitably will), it's worth taking a hard look at your budget and determining whether it aligns with your current reality.

That means:

- Adjusting the percentages if needed

- Revisiting your budget monthly

- Letting it change as your income or priorities change

Some months will be tighter than others.

Some goals will move faster than expected. That’s normal.

From budgeting to habits

You now have something powerful: goals that matter to you, and a budget that supports them.

But plans don’t live on paper.

They live in the small decisions you make every day.

In Part Five, we’ll look at money habits.

The quiet, repeatable behaviours that determine whether this plan becomes something you live by, or something you forget about.

Because lasting change doesn’t come from big moments.

It comes from small actions, repeated gently over time.

And you’re already building them.