22/1/26

What I Spent This Week as a Freelance Marketing Consultant Making £43k

Ever wondered how others really manage their money?

Ever wondered how others really manage their money?

In the A Week in My Wallet series, we share it all, because talking about money shouldn't be off-limits.

Every week, an anonymous member shares a week of their spending: no names, no filters, just honest stories about life's everyday financial choices.

Ready to join the conversation and help make money talk less taboo? Share your own story via our form here.

Assets (e.g. investments, owned property, other):

I own my apartment in Berlin, which I cashed out 10 years ago, when I bought it with my savings and by selling my stocks from my employer in the UK where I worked for 7 years. At the time of buying the apartment I benefited from a good exchange rate (pound to euro).

Other assets, my portfolio which I'm slowly building up. I started 1.5 years ago when I lost my job and received severance and I became a single mum at the same time. My ex started investing (while I was pregnant) with his own capital, so he was the main influence at the time.

When I realised I will lose my job (to a man who covered my maternity leave) and receive a year worth of salary, I started learning about investing (books, webinars on female invest, talking to friends who are trading or investing).

I invested about €45,000 (£38,700) so far and I have a decent return on that about 17% which is not realised gain.

The reason for this above average gain so far is that I started investing in semi conductors (AI related stocks) in 2024. This is paying off, but if the AI bubble really bursts, I will have a problem. I am currently working on my diversification and risk management.

I also found out that I have a private pension fund back in the UK where Ive been paying in some part of my salary while at my job in the UK, and I joined the pension plan as a colleague of mine said I should do it cause “it's free money” with my ex-employer matching individual contributions.

I can't access these funds until I'm 57, but at least they are still growing and for the first time when I log in, I understand how they are being invested.

Monthly Take-Home Pay (after tax): About €3,000 (£2,580)

Do you share expenses with someone?

No but I have a small child living partly with me, and I receive his child benefit (€255 / £219.30) and his father contributes €100 (£86) towards the health insurance which is a huge expense in Germany.

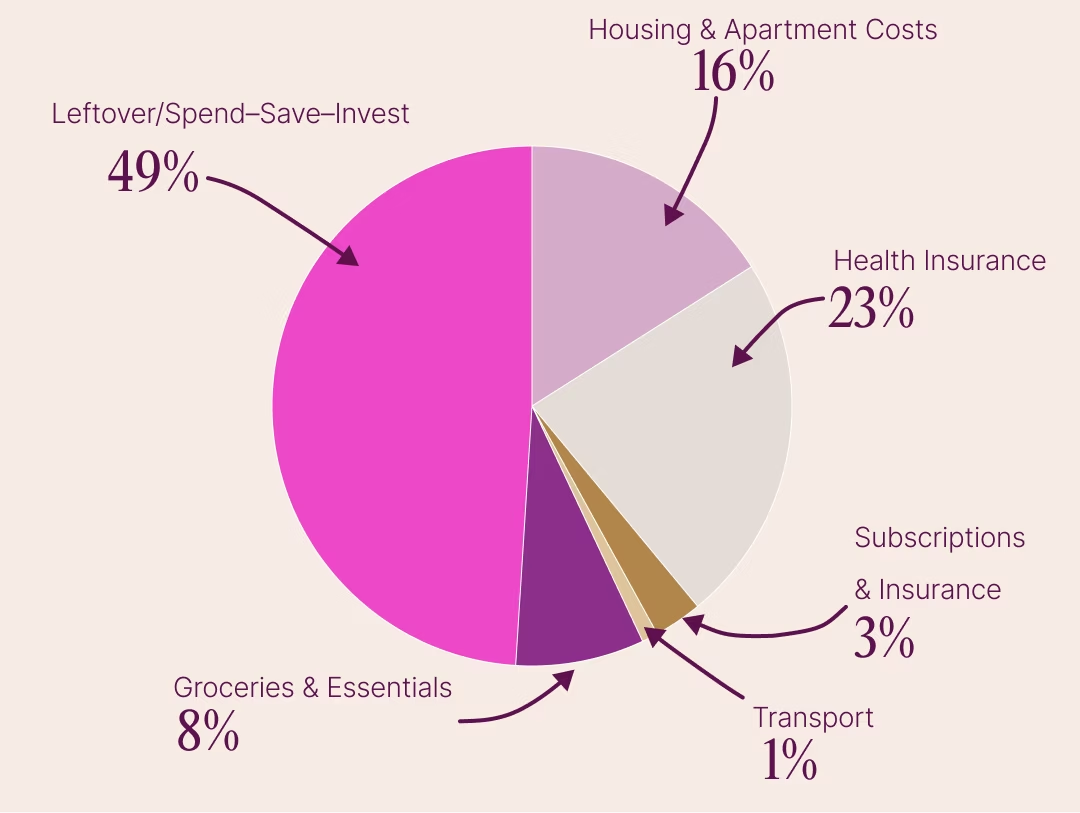

What is your overall monthly budget?

- No rent/mortgage, but my monthly apt outgoings for the building maintenance etc. and bills (electricity, internet, tv license) come to about €600–€650 (£516–£559) per month.

- I pay €912 (£784.32) as a freelancer for health insurance (yes, ouch).

- Other subscriptions, €59 (£50.74) for the gym pass. €23 (£19.78) for ChatGPT Plus which I can put through as a business expense as a freelancer.

- And some other insurance costs like household insurance and family law insurance (about €30 (£25.80) per month).

- Transport: €20–€50 (£17.20–£43) for public transport per month only as I use the bike for part of the year or I don't go too far from home (and Iive pretty centrally)

- Groceries & essentials: probably about €300 (£258) per month.

- Investment contributions: sometimes several thousands if its a good month for market dip opportunity. Sometimes only a couple of hundreds. I don't have savings plans set up as I have only a few ETFs but mainly individual stocks (not more than 15).

Amount left each month after essentials (to spend, save or invest):

Around €2,000 (£1,720). I try to save/invest €1,000–€1,500 (£860–£1,290) per month and the rest is play money, occasional dinner out, toys for my son, family or a trip from time to time, upgrades to my apt, some clothes, and so on.

Dependents (if any): Yes, one 4 year old boy.

My relationship with money

Growing up, did your parents or guardians educate you around money?

I come from an upper middle class family from a war country (so in western terms, this is more like lower middle class). This means my family went through everything, hyper inflation, sanctions, etc. yet, we always scraped up here and there and had enough to at least invest in my education abroad.

I had to work during my studies to be able to pay the rent in London. I sometimes did 2–3 jobs next to studying full time. What this taught me is the value of money when you work for it from a very young age (as opposed to money being given to you).

I was always good at saving, and finding ways to make a buck. My mother is super risk averse. She cant even hear about the stock market. But she is the bread winner in my family and in that sense a role model.

I think I risk more with my investments than my parents (they think property is the safest option) but I am also on the cautious side with my portfolio, and I got burnt now enough times seeing how some of my invested money is melting away cause I didn't do proper risk management and research.

The good thing is, I still got time on my side so hoping those reds will go into greens eventually.

What was your first job and why did you get it?

I worked on TV as a kids tv presenter and I never got paid for it, until my great grandma told the producer to not call any more 😆 Then I worked as a radio host and I made some pocket money in my high school.

Then during my studies I worked as a shop assistant in Jigsaw and then as a gym receptionist for a little over minimum wage in London. But it was the best student job ever.

Did you worry about money growing up?

Yes, as a child of divorced parents who were always fighting who will pay for what over my shoulders, I wanted to be financially independent as soon as possible. Plus I felt bad to ask for more money during my studies as I knew how hard it was for them to scrape up to pay for my tuition as an international student in London.

At what age did you become financially responsible for yourself and do you have a financial safety net?

You could say it was around the time when I started studying, as I covered all living expenses from my part time jobs but my parents paid the Uni tuition, so about 19. I was almost 22 when I graduated and got my first, terribly paid job in a media agency.

Financial safety net – well, yes, my savings.

Do you worry about money now?

Yes, now I have a child, unstable freelance job, (since I was laid off) and my ex also doesn't have a stable income so, I often feel like its all on me to sustain the family (I don't support him and he doesn't support me, but we try to equally contribute for our son).

What is your biggest money regret?

For some time in recent years in Germany I let my savings just lose value due to inflation, as there is no such thing as Cash ISA here. I was too busy with my job and then having a baby, and I missed out on some high interest rates for some years. Not to mention putting some of that money earlier into an ETF at least. I didn't have the knowledge that I have now about the way markets work.

What financial goals are you working towards?

Complete financial independence by the time I'm 50. Make work optional so I can focus more on raising my son to be a good man.

Who is your financial role model (if any), and why?

Generally speaking, all women who don't depend on their husbands/partners for their finances. And those women who have the courage to start their own businesses.

Reflections on my Spending Habits:

It's mainly about necessities and very little treats for me. I should live a little. 😆

To explain the attached photo below, it was Orthodox Xmas this week, it is customary to bake a bread and put a coin inside and then distribute pieces of bread amongst the family members. Then who ever gets the coin is the “bread winner” this year. Or in other words will have a good financial year. Luckily I got the coin this year.

What I Spent in a Week

Day 1 – Monday: €34.25 (£29.45)

• Groceries: €27 (£23.22)

• Korean face masks: €6.5 (£5.59)

• Pharmacy (vitamin D supplements): €9.75 (£8.39)

Day 2 – Tuesday: €52 (£44.72)

• Breakfast pastry and groceries: €12 (£10.32)

• Contribution to a friend’s 40th birthday present: €40 (£34.40)

Day 3 – Wednesday: €0 (£0)

• No spending

But I invested €180 (£154.80) into my Silver ETC as it was down 5.8% that day

Day 4 – Thursday: €16 (£13.76) (excluding investment)

• Contribution to a friend’s funeral: €13 (£11.18)

• Cleaning products: €3 (£2.58)

I invested another €180 (£154.80) into Silver ETC as it went down a bit more and I believe it will continue growing this year

Day 5 – Friday: €47 (£40.42)

• Cleaning lady: €32 (£27.52)

• Toiletries (DM): €15 (£12.90)

• Takeaway lunch: €10 (£8.60)

Day 6 – Saturday: €23.76 (£20.43)

• Groceries: €13.26 (£11.40)

• Coffee beans: €10.50 (£9.03)

Day 7 – Sunday: €8 (£6.88)

• Takeaway dinner: €8 (£6.88)

Total Weekly Spend: €181.01 (£155.67)