22/1/26

What I Spent This Week as a Lawyer making $100k

Ever wondered how others really manage their money?

Ever wondered how others really manage their money?

In the A Week in My Wallet series, we share it all, because talking about money shouldn't be off-limits.

Every week, an anonymous member shares a week of their spending: no names, no filters, just honest stories about life's everyday financial choices.

Ready to join the conversation and help make money talk less taboo? Share your own story via our form here.

Monthly Take-Home Pay (after tax): £3,800 ($5,092)

Do you share expenses with someone? No

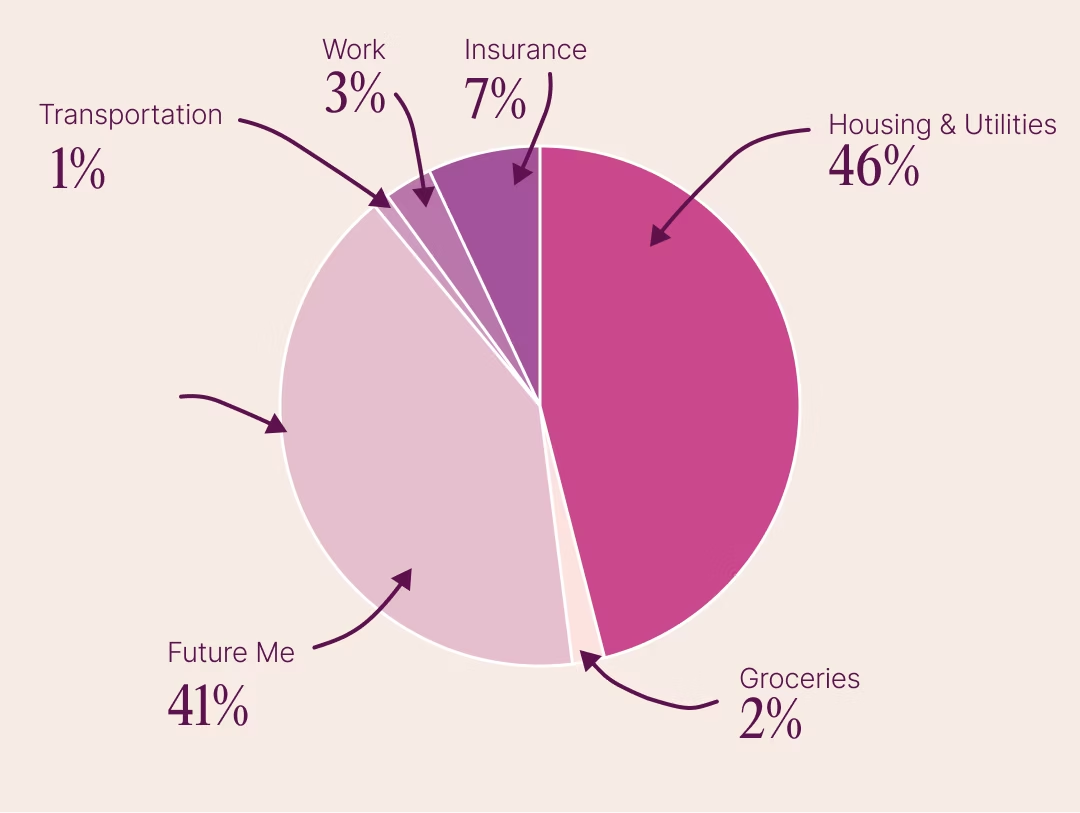

What is your overall monthly budget?

- Mortgage: £1,500 ($2,010) (includes £170 ($227.80) voluntary overpayment)

- Bills: £650 ($871)

- Transport: £250 ($335)

- Groceries: £100 ($134) (I travel frequently for work and food expenses are often covered)

- Miscellaneous: £200 ($268)

Amount left each month after essentials (to spend, save or invest): £800 ($1,072)

Dependents (if any): None

My Relationship with Money

Growing up, did your parents or guardians educate you around money?

Not specifically - my mum would always say it’s important to keep a £5 note in your purse at all times in case of emergency, but that’s about it.

What was your first job and why did you get it?

I went straight into law after finishing university. Growing up, my parents were against me having a part-time job and said my only job was to get good grades and worry about working for the rest of my adult life afterwards.

Did you worry about money growing up?

Not really, my parents worked really hard and we grew up comfortably - at least that’s how it seemed. In reality, my parents earned good salaries but had little savings and kind of lived hand to mouth, making sure we had what we needed. We’re quite fortunate we never had any extreme emergencies pop up that couldn’t be dealt with in the short term.

At what age did you become financially responsible for yourself, and do you have a financial safety net?

I lived at home with my parents for the first few years once I started working which really helped me building up a savings pot (and eventually buy my own house). Whilst I home I would contribute to groceries but I became fully financially responsible for myself at 25 when I began living independently.

Do you worry about money now?

Yes, even though I have a good salary, everything feels expensive and being single means I feel acutely aware that I need to be in a good financial position at all times, because it’s only me that can take care of things if anything goes wrong. However, I appreciate I’m in a really good position and have the ability to cut back on certain expenses if I need to. I’ve chosen the lifestyle I have (e.g. buying a house with a high mortgage) and feel comfortable with those choices.

What is your biggest money regret?

Not saving/investing sooner!! I was initially self-employed and was overwhelmed by the vast information on pensions, so I naturally did nothing to set aside money into a pension.

I only opened up my LISA two years into working life, and that’s potentially £2,000 of free government money that I missed out on (plus all that compound interest). But, better late than never.

What financial goals are you working towards?

Build up my savings (I put extra towards my house deposit out of my emergency funds and move in costs) and continue maxing out my LISA. I currently have a five year fixed mortgage and want to keep making overpayments, increasing them as my salary increases.

Who is your financial role model and why?

My sister - she paid off her (plan 1) student loan in less than 10 years I think, paid for her masters and MBA, and generally is good with saving money but also enjoying life experiences. When I turned 25 and got a new job, I wanted to spend some of my savings on a designer bag. She convinced me to use the money to instead pay off a loan for postgraduate studies early. I didn’t agree with her at the time, but glad I listened to her advice. I paid that loan off 24 months early and saved about £2,000 in interest.

Reflections on my Spending Habits:

I was able to put quite a bit extra into savings and clearing debt because of a work bonus. I feel like I’ve spent it wisely.

What I Spent in a Week

Day 1 – Monday: £200 ($268)

• Credit card repayment: £200 ($268)

Day 2 – Tuesday: £141 ($189.00)

• Groceries: £60 ($80.40)

• Life insurance: £75 ($100.50)

• Parking for work: £6 ($8.04)

Day 3 – Wednesday: £3,061 ($4,101.74)

• Stocks and shares ISA contribution: £50 ($67)

• Mortgage payment: £1,500 ($2,010)

• Income protection insurance: £55 ($73.70)

• Parking: £6 ($8.04)

• Savings transfer: £1,000 ($1,340)

• Additional savings transfer: £450 ($603)

Day 4 – Thursday: £355 ($475.70)

• Microsoft Office package: £105 ($140.70)

• House renovation contribution: £250 ($335)

Day 5 – Friday: £18 ($24.12)

• Parking for work: £18 ($24.12)

Day 6 – Saturday: £0 ($0)

• No-spend day (I have it in my calendar as a no-spend weekend)

Day 7 – Sunday: £0 ($0)

• No-spend day (I have it in my calendar as a no-spend weekend)

Total Weekly Spend: £3,775 ($5,058.50)