5/11/25

A true Halloween horror on the financial markets – with China, the U.S., and the tech giants in starring roles

The trade war between China and the U.S. haunted investors, concerns about an AI bubble grew, and the sharp rally in gold came to an abrupt

October turned into a real thriller on the financial markets.

The trade war between China and the U.S. haunted investors, concerns about an AI bubble in the stock market grew, and the sharp rally in gold and silver prices came to an abrupt halt.

At the U.S. Federal Reserve, Chair Jerome Powell was groping around in the dark.

The world’s largest economy has been partially paralyzed by a government shutdown after lawmakers failed to agree on a new budget.

Thousands of public employees have been sent home – including those responsible for delivering the monthly jobs report and inflation figures, two of the Fed’s most crucial indicators for interest rate decisions.

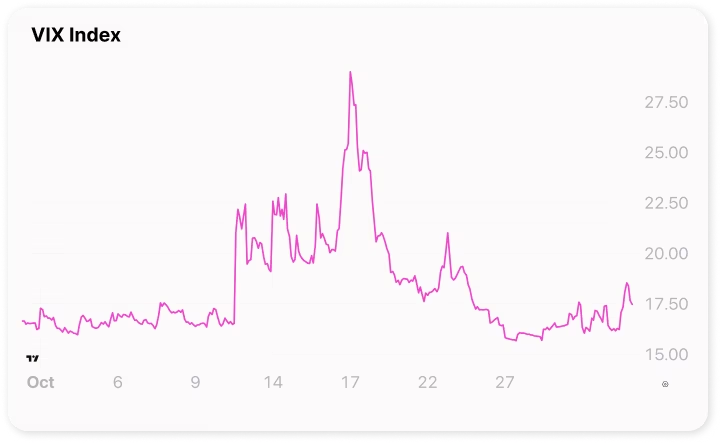

Investor fear peaked mid-month, when the VIX Index (Volatility Index) jumped from 15 to 25 percent.

Toward the end of the month, optimism returned as investors began to believe in the prospect of a trade deal between Presidents Xi and Trump, and it seemed Powell might be navigating towards a rate cut.

All we needed then were strong earnings from the heavyweight U.S. tech companies so the AI balloon – and the markets – could lift even higher.

Whether the month ended with tricks or treats for investors, we’ll get back to that.

First, let’s turn to Asia – where one woman sent Japanese stocks soaring to new records, while President Xi gathered his top team to chart the course for China’s – and the global economy’s – future.

Japanese Stock Rally Gains Momentum

Mid-month, Sanae Takaichi was surprisingly elected as the new leader of Japan’s ruling LDP party. Just a few days later, she was appointed Japan’s first female Prime Minister.

Takaichi has promised fiscal stimulus to give a boost to the world’s fourth-largest economy. Japan is lagging behind on both green and digital transitions and has lost competitiveness relative to countries like China and South Korea.

The 64-year-old Takaichi is a political protégé of former Prime Minister Shinzo Abe (2012–2020). Following the financial crisis, Abe implemented significant fiscal and monetary easing in Japan – a strategy that helped the Nikkei index nearly double over his tenure.

Investors now see the potential for a new round of “Abenomics” under Takaichi, which has further accelerated the Nikkei index, comprised of 225 companies including SoftBank, Sony, and Teradyne, listed on the Tokyo Stock Exchange. Over the past month, the index has climbed nearly 16 percent.

The positive sentiment in Japan is reflected across East Asia. South Korea’s KOSPI index is up 71 percent for the year, China’s Hang Seng has gained 32 percent, and Taiwan’s index is up 23 percent.

By comparison, the benchmark U.S. S&P 500 is up 16 percent for the year, supporting the narrative that investors are increasingly looking for alternatives to American equities.

China Charts the Course for Our Future

We stay in Asia. While the U.S. President has been busy with a peace plan for Gaza, building a ballroom at the White House, and firing off tariff threats at Canada and China on social media, the Chinese President has been quietly gathering his top officials at the Jingxi Hotel in Beijing.

There, they have calmly been setting the course for "The Middle Kingdom” over the next five years.

And when China makes plans, the ripple effects are felt across the global economy.

China’s new five-year plan for 2026–2030 (the 15th in the series) will officially be presented at the National People’s Congress next March.

But we already know that China is aiming – and making significant progress – to become a technological and green superpower with a high degree of self-sufficiency.

China’s ambitions are no secret to the U.S. President, who is particularly focused on curbing China’s dominance in strategically critical rare earth elements – a group of 17 metals that play a key role in modern technologies, from AI to the green transition and defense industries.

These rare earths are also central to the trade war between China and the U.S.

This was evident on Friday, October 10, when Trump threatened 100% additional tariffs on Chinese imports to the U.S.

The threats followed China’s tightened control over rare earth exports, where the country accounts for 90% of global production – and holds the most advanced processing know-how.

By Sunday, however, the U.S. President was already posting conciliatory messages on his social media platform, Truth Social.

Crucial Meeting Between Xi and Trump

In the last week of the month, the two leaders held their first face-to-face meeting since 2019 at the APEC summit in South Korea.

The meeting lasted around one hour and forty minutes and resulted in a one-year agreement: the U.S. will reduce tariffs on Chinese goods from roughly 57% to 47%, while China abandons its planned export restrictions on rare earth elements.

In his usual style, Trump described the meeting as “fantastic” and gave it a rating of 12 out of 10. Xi, for his part, emphasized that economic tensions between the countries are “normal” and can be “managed through dialogue and mutual respect.”

However, China still controls 90% of global rare earth production. This means Xi could, at any time, disrupt U.S. and European tech production – or at least seriously interfere with supply chains.

The U.S., meanwhile, holds the most advanced AI chips, but China is rapidly catching up, driven in part by companies like Alibaba and Huawei Technologies.

So while Xi and Chinese companies want access to the lucrative U.S. market, China still holds the strongest cards.

Solid Chinese export figures in October also demonstrate that the Chinese economy remains resilient despite American tariffs.

Analysts view the deal as a tactical move rather than a lasting solution to the deeper conflicts between the U.S. and China. “This is not a trade peace, but rather a necessary breathing space,” one economist told Reuters.

Central Bank Gropes in the Dark

The day after the China-U.S. trade deal was finalized, investors turned their attention to another major event: The Federal Reserve interest rate meeting.

The lead-up to the meeting was dramatic.

At the time of writing, U.S. public sector employees had been furloughed without pay for four weeks, as Washington lawmakers failed to agree on the budget for the coming year.

Americans are no strangers to government shutdowns; they typically last just over a week. The longest shutdown so far occurred in 2018 and lasted 35 days.

As a result, the Fed had to make its rate decision without key employment data, simply because there were no staff available to compile it.

The Fed delivered its second rate cut of the year: 0.25 percentage points, exactly as the market had expected.

However, at the subsequent press conference, Chair Jerome Powell tempered investor expectations for another cut in December. At the September meeting, he had signaled two more cuts for the year.

Consequently, the S&P 500 did not rise, as it typically does following a rate cut.

A Bitter Taste in Metals

In October, gold prices hit $4,000 per troy ounce for the first time, marking a gain of over 50% for the year.

The surge has been driven by uncertainty surrounding the world’s largest economy, U.S. interest rate cuts, central bank gold purchases, geopolitical tensions, and FOMO (fear of missing out) among investors.

On October 20, gold suffered its largest drop since 2020, falling 6.3%, while silver fell just over 7%. Silver’s larger drop compared to gold reflects differences in liquidity – the silver market is roughly nine times less liquid than gold, amplifying both rises and falls.

What caused the drop?

- Profit-taking: After a long rally, many investors wanted to lock in gains, especially after gold failed for the third time to break above $4,400.

- Improved U.S.-China relations: A softer tone between the two superpowers reduced demand for “safe-haven” assets like gold and silver, sending risk-tolerant investors back into equities.

- Seasonal factors: The decline came ahead of India’s Diwali festival and wedding season, which this year generated strong demand in the preceding weeks.

That said, the structural factors behind this year’s historic gains remain intact, continuing to support metals that are still underrepresented in global portfolios.

A Mixed trick-or-treat bag

The debate over whether the AI boom is tipping into bubble territory is intensifying.

In October, chip giant Nvidia became the first company ever to reach a $5 trillion valuation. At the same time, rumors surfaced that OpenAI is laying the groundwork for a potential IPO in 2027 – possibly the largest ever, with an estimated valuation of around $1 trillion.

It’s hard not to see parallels with the dot-com era: Skyrocketing valuations, inter-company trades between tech giants and chipmakers, and a growing reliance on debt-fueled growth.

The final 48 hours of October proved crucial for market sentiment, as earnings reports from the five tech giants – Microsoft, Meta, Amazon, Apple, and Alphabet (Google’s parent company) – were released.

The numbers were strong. Amazon, in particular, surprised investors with robust results, while Apple delivered better-than-expected iPhone sales. Taken together, the five reports supported the argument against an AI bubble, showing that these companies still have solid earnings.

However, announcements from Meta and Microsoft about even larger investments in artificial intelligence raised questions about whether these companies are paying too much for growth.

That question remains the biggest risk for the tech sector. There is no clear answer yet, and investors will be looking for clues in November, when Nvidia releases its earnings report mid-month.