2/9/25

Oil Shocks, Trade Wars, and Billionaire Breakups: June’s Economic Rollercoaster

Markets kicked off June with a surge of optimism, largely driven by speculation about trade discussions between the US and China.

Markets kicked off the summer with a surge of optimism, largely driven by speculation about trade discussions between the US and China.

However, throughout the month, we've seen a potent mix of trade tensions, global high-level summits, and geopolitical unrest centered in the Middle East, along with a series of central bank meetings. On the sidelines, there was also the dramatic breakup between the US President and Elon Musk.

Below, you can see the fluctuations in the S&P 500 index over the past month.

The easing of rhetoric between China and the US is reflected in the market's rise, which began around June 6th. From June 13th onward, the situation in the Middle East has been the primary factor influencing investors.

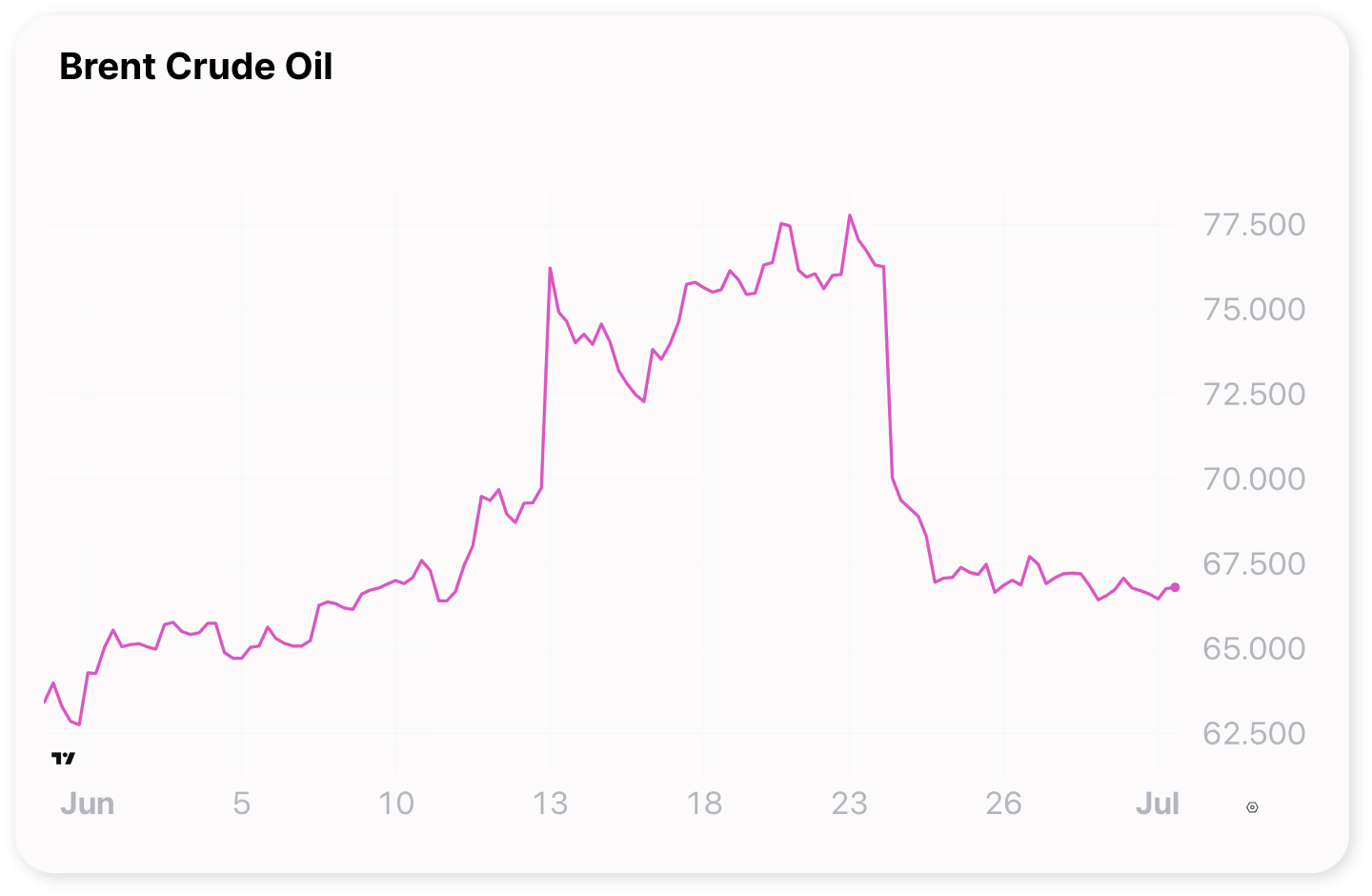

Middle east tensions spark oil shock

The situation in the Middle East escalated sharply on the night of Thursday, June 12th, as Israel deployed approximately 200 bombers and fighter jets against Iran. The primary target was the city of Natanz, home to Iran's nuclear program headquarters. In the following days, Israel and Iran exchanged attacks, resulting in the deaths of several high-ranking Iranian officials and nuclear scientists.

The most significant market reaction occurred in the commodities sector.

Brent crude oil prices surged by 7%, reaching $73 per barrel – the largest increase since Russia's invasion of Ukraine.

This rise was primarily driven by concerns over potential disruptions to oil supplies through the critical Strait of Hormuz, a vital chokepoint for global oil trade. Roughly 20% of the world's oil passes through this strait. Should Iran choose to block this route, even temporarily, it could lead to a dramatic surge in oil prices.

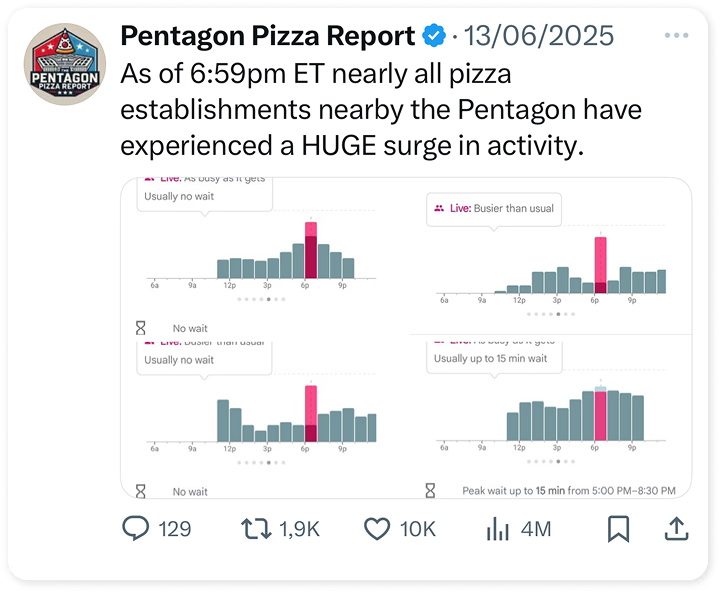

All eyes then turned to the United States – or rather, to the number of pizza orders at the Pentagon.

Roughly an hour before Iranian state television reported Israeli explosions in Tehran on June 13th, pizza orders around the Pentagon surged dramatically.

This was reported by X user Pentagon Pizza Report, a source that, according to The Guardian, has previously been used to predict significant political events like the 1989 U.S. invasion of Panama and the 1991 Kuwait War.

This prompted President Trump to leave the critical G7 summit in Canada, involving the world's largest economies, to convene in "The Situation Room" at the Pentagon.

On June 22nd, the U.S. launched an attack on three missile facilities in Iran. By the 24th, Trump announced a negotiated ceasefire, which both Iran and then Israel accepted.

As of this writing, the ceasefire has held for three hours, and looking at oil prices, it appears market participants have somewhat calmed down.

However, there's a significant difference between a ceasefire and a formal peace agreement.

For now, it seems international shipping and trade can proceed unhindered through the crucial Strait of Hormuz.

Deadline for tariff negotiations looms

Moving from the conflict in the Middle East, we now turn to the front lines of the trade war between the US and the rest of the world.

During the first weekend of June, at a steel plant in Pennsylvania, Trump held a rally where he announced a doubling of tariffs on foreign steel, from 25% to 50%.

This move aimed to protect American jobs in the steel industry, demonstrating that the U.S. President was not going to wait for the EU, China, Canada, and others to make their proposals for tariff negotiations.

The following weekend, a Chinese delegation met with a US delegation in London. After 20 hours of negotiations, they reached a trade agreement. This agreement reportedly includes a 55% tariff on Chinese goods imported into the US, and conversely, a 10% tariff on American goods entering China.

Additionally, China is reportedly prepared to lift restrictions on the export of magnets and rare earth elements – a major bargaining chip for Chinese President Xi.

Trump was quick to announce the successful negotiations, calling his relationship with China's President "excellent."

If you're wondering why financial markets have only reacted with moderate enthusiasm, it's because the details of the agreement and a formal signature have not yet been seen.

Perhaps more importantly, the Chinese have not yet confirmed the agreement.

Therefore, the trade negotiations are still very much "game on." The only signature currently in place is for an agreement between the United Kingdom and the United States, indicating there's still a long way to go. And this won't conclude by July 9th; that date will simply be a preliminary marker.

A $150 billion breakup

Trump hasn't only been busy with his relationship with the Chinese President.

As you can see from the graph below showing Tesla's share price performance, the former "bromance" between the U.S. President and the world's richest man took a hit this month.

Specifically, it experienced a 14.26% decline.

On their respective social media platforms – X and Truth Social – Elon Musk and Trump engaged in a verbal spat that escalated on Thursday, June 6th.

In the days leading up to this, Musk had criticized Trump's tax package ("Big, Beautiful Bill"), which Musk called a "disgusting abomination."

Musk might have seen investment bank JP Morgan's statement that if the package were to pass in its current form, it could potentially reduce Tesla's bottom line by $1.2 billion in 2025.

From there, the situation spiraled.

Trump threatened to remove government support and contracts for Musk's companies, including Tesla and SpaceX. Elon Musk retaliated by claiming Trump's name should appear in cases related to the late financier and convicted sex offender Jeffrey Epstein.

This public exchange cost Tesla shareholders approximately $150 billion in lost market value in a single day.

Over the weekend, however, both individuals somewhat cooled down. Trump announced that he had no plans to get rid of his red Tesla and no intentions of stopping collaboration with Starlink.

Elon Musk deleted several of his posts on X and wrote: "I regret some of my posts about President Trump last week. They went too far."

I regret some of my posts about President Trump last week. They went too far

While their reconciliation has been good for Tesla's stock price, Musk is out of the DOGE Ministry (Department of Government Efficiency), and he has been ousted from the U.S. President's inner circle.

This serves as a clear example that if you're not 100% with Trump, you're against him.

U.S. Federal Reserve holds interest rates steady

While discussing Trump's relationship management, let's briefly touch upon the U.S. Federal Reserve (FED). Trump has long used harsh words for FED Chair Jerome Powell, advocating for interest rate cuts.

However, at its mid-June meeting, the FED, as expected, kept interest rates steady in the 4.25-4.50 percent range. Trump subsequently settled for calling Powell "a very stupid person."

Perhaps this is because Powell's term as chair ends next year, and Trump has already put forward a candidate who is 100% aligned with him.

The central bank still anticipates two interest rate cuts later this year. However, they've lowered their growth forecast and raised their inflation expectations.

The FED now projects average inflation this year to be around 3%, which is 1% above their target, primarily due to Trump's retaliatory tariffs.

Global economic slowdown

The fear is that the U.S. economy could enter a scenario of both declining growth and rising prices (stagflation).

U.S. inflation saw a slight increase in May to 2.4 percent. The labor market continues to advance, though at a slightly slower pace.

Over the past three months, an average of about 150,000 new jobs have been created each month, which is acceptable but not the strong figures we are accustomed to seeing.

Other key economic indicators have also come in a bit weaker over the past month. Retail sales fell by 0.9% in May, and industrial production dropped by 0.2%. This collectively suggests that the U.S. economy has downshifted following Trump's tariff actions on April 2nd.

In line with the IMF (International Monetary Fund) and the World Bank, the OECD also weighed in this month with a downward revision to global growth forecasts.

As quoted by OECD Secretary-General Mathias Cormann: "The global economy has shifted from a period of robust growth and declining inflation to a more uncertain path."

The global economy has shifted from a period of robust growth and declining inflation to a more uncertain path

The U.S., Canada, Mexico, and China are expected to be particularly affected.

However, we can take comfort in the OECD's projection that GDP growth in the Eurozone will increase to 1% this year and 1.2% in 2026, up from 0.8% last year.

Interest Rate Cut as Growth Rocket

At the European Central Bank (ECB) interest rate meeting on June 6th, President Ursula von der Leyen indeed opted to cut the interest rate by 0.25 percentage points for the eighth consecutive time.

Simultaneously, the average inflation forecast for the Eurozone was lowered from 2.3% in 2025 to 2%, which is precisely where the ECB aims for it to be.

As Europe still significantly needs an economic growth boost, financial markets anticipate further rate cuts from the ECB in the latter half of the year. Von der Leyen may consider the PMI (Purchasing Managers' Index) data for the entire second quarter, which indicates that the Eurozone economy has slowed down. PMI measures the future expectations of purchasing managers in businesses, and these expectations are declining.

The roller coaster theme of recent months looks set to continue. This is also one of the reasons why gold prices continue to set new records, as investors traditionally seek refuge in gold during periods of turbulence in financial markets.

Looking at the VIX (the Fear Index), it surpassed the crucial 20-point threshold, signaling increased uncertainty, in the middle of the month. However, it seems we will end the month where we began, around 18.

Market sentiment, however, could quickly be influenced by the situation in the Middle East, Trump's tariff deadline on July 9th, and, as of June 24th when this article concludes, an important NATO summit has just begun in The Hague.

It was at the NATO meeting in February that Europe realized it was "alone at home," and that it might not be able to fully rely on the United States to stand firmly with Europe going forward.

What is certain is that the EU will further increase defense budgets, and there are reports that the individual countries might raise defense spending and armaments to as much as 5% of their GDP.

This suggests even more momentum for defense stocks, cybersecurity, and communication sectors. Furthermore, an exciting earnings season awaits at the end of July, where technology companies will once again be in focus.