29/6/26

What I Spent This Week as a Senior Frontend Developer Making $79K

Ever wondered how others really manage their money?

Ever wondered how others really manage their money?

In the A Week in My Wallet series, we share it all, because talking about money shouldn't be off-limits.

Every week, an anonymous member shares a week of their spending: no names, no filters, just honest stories about life's everyday financial choices.

Ready to join the conversation and help make money talk less taboo? Share your own story via our form here.

Monthly Take-Home Pay (after tax): €4,082 ($4,613)

Do you share expenses with someone? Yes, with my husband

Household Income (if shared): €145,000 ($163,850)

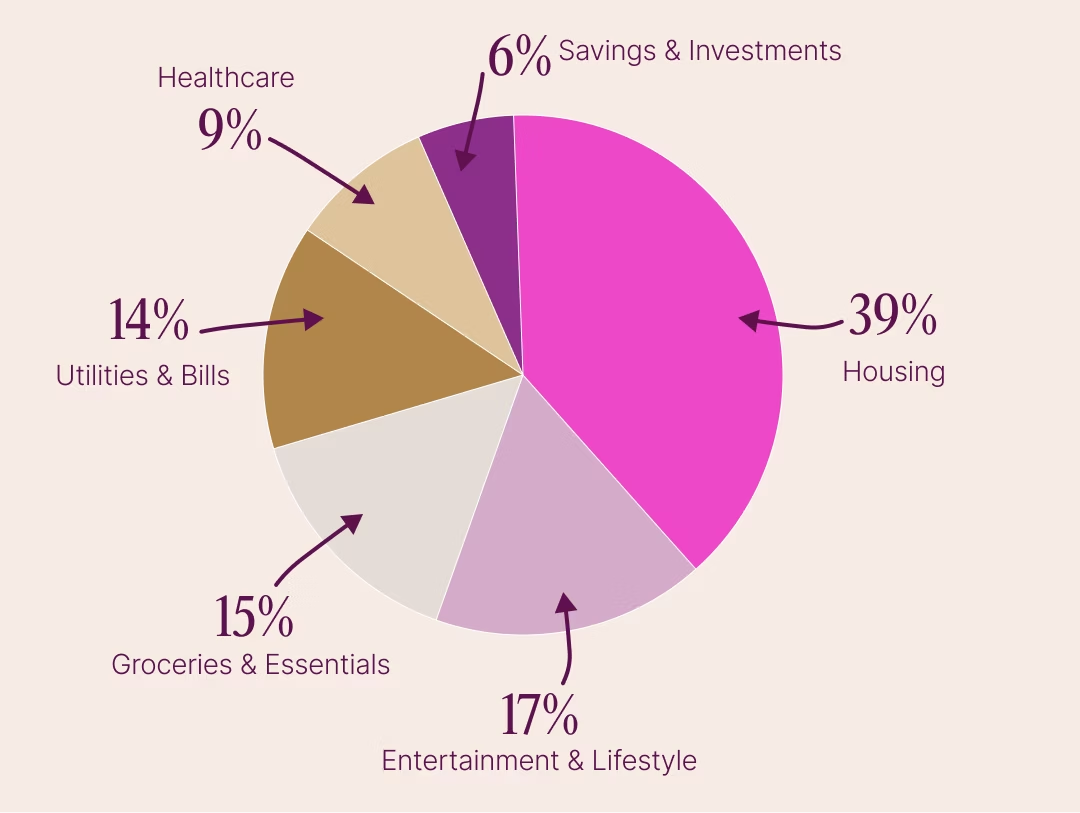

What is your overall monthly budget?

All house expenses are shared with my husband:

- Mortgage €1,403 ($1,585)

- Bills and house expenses €504 ($570)

- Groceries €500 ($565)

- Restaurants €250 ($283)

- Health insurance €333 ($376)

My own expenses:

- Monthly investment around €200 ($226) a month

- Phone subscription €12 ($14)

- Clothing budget €300 ($339)

- Restaurants and lunches €50 ($57)

- Essentials €50 ($57)

Amount left each month after essentials (to spend, save or invest): Around €2,000 ($2,260)

Dependents (if any): n/a

My Relationship with Money

Growing up, did your parents or guardians educate you around money?

Growing up, my parents valued money deeply and worked incredibly hard to build their wealth. The most important lesson they passed on to me was to never borrow money, to live within your means and earn what you spend.

From a young age, I was given real responsibility around money. As a small girl, I was often trusted with the task of counting the cash they earned from their business. Looking back, this was more than just a chore, it was a hands-on financial education. It taught me that money represents effort, time, and dedication. Because of this, I developed a genuine appreciation for the value of money and the discipline it takes to build it.

That said, the financial education I received was somewhat old-fashioned. It was rooted in caution and tradition: save what you have, never borrow, and keep money close. My dad did invest, but primarily in property, which was very much the traditional route of his generation. There was little conversation about other ways of growing wealth, such as stocks, funds, or financial markets. The focus was on tangible, physical assets rather than the broader world of investing.

At the same time, growing up in a household where money was a constant focus gave me an important perspective. I noticed that the pursuit of financial security could sometimes overshadow the simple joys of everyday living. This shaped me in a meaningful way, in my own life, I actively try to honour the financial discipline my parents modelled, while also making space to enjoy life as it unfolds, rather than always chasing the next financial goal.

So in short, my upbringing gave me both a strong foundation in financial responsibility and the awareness that money is a tool for living well not an end in itself.

What was your first job and why did you get it?

I started out helping in my parents’ business as a cashier, which gave me my first real experience dealing with customers and handling responsibility. Later, I worked in hospitality because I wanted to earn my own money, become more independent, and save up for travelling.

Did you worry about money growing up?

Not really. I was always able to ask for the essentials, and I could earn some of my own money by helping out. If anything, my main worry was that my parents’ focus might sometimes be in the wrong place.

At what age did you become financially responsible for yourself and do you have a financial safety net?

From around 19, I started earning my own money for extra spending. After finishing my studies, at around 25, I became fully independent and started living on my own. While I support myself, I know I can rely on my family and husband if needed, which gives me a sense of security.

Do you worry about money now?

Working in tech does make me think about what the future might bring, so in the long term, yes. But on a day-to-day basis, I feel comfortable and financially stable.

What is your biggest money regret?

I regret not starting monthly investing earlier in my career. Because of that, I probably spent more money on things I didn’t really need at the time.

I did invest in important things like my house and wedding, which I don’t regret, but overall my savings account doesn’t look as strong as I would have liked.

What financial goals are you working towards?

I’m focused on building my savings based on the “F*** You Fund” approach, while continuing to invest monthly. The goal is to create more financial freedom and long-term security.

Who is your financial role model (if any), and why?

I’ve learned a lot from my parents, especially when it comes to work ethic and managing day-to-day finances. Currently, I really value my husband’s knowledge on investing, as well as how thoughtful and careful he is with spending money.

Reflections on My Spending Habits:

I usually don’t spend much on small, day-to-day things, but when I do spend, the amounts tend to be higher.

What I Spent in a Week

Day 1: Monday - €165 ($186)

• €55 ($62) — Monthly yoga subscription

• €40 ($45) — Tickets for an event with friends

• €70 ($79) — Groceries

Day 2: Tuesday - €26 ($29)

• €26 ($29) — Beauty and pharmacy

Day 3: Wednesday - €54.99 ($62)

• €45 ($51) — Yoga workshop

• €9.99 ($11) — Bank fee

Day 4: Thursday - €118 ($133)

• €40 ($45) — Train

• €78 ($88) — Home insurance

Day 5: Friday - €53.75 ($61)

• €50 ($57) — Drinks and dinner with friends

• €3.75 ($4) — Bakery

Day 6: Saturday - €243 ($275)

• €170 ($192) — Stocking up on groceries

• €73 ($82) — Dinner with friends

Day 7: Sunday - €0 ($0)

• €0 ($0) — Nothing spent on this day.

Total Weekly Spend: €660.74 ($747)