2/9/25

Trade Tensions & Tariff Whiplash: Trump’s First 100 Days

Trump’s “Liberation Day” rattled markets, sparked US-China trade fears, and kicked off a volatile earnings season.

In April, Donald Trump's 'Liberation Day' essentially sidelined many market indicators investors rely on. The spotlight has been on tariffs and the repercussions of a rapidly escalating trade war between the world's two largest economies – the US and China. We've also witnessed a significant breakdown in trust between the American economy and the rest of the globe, and the starting gun has fired for an almost too-exciting Q1 earnings season.

Tariffs Is The Most Beautiful Word

The financial markets experienced a landmark month in April 2025. On April 2nd, President Trump's announcement of tariffs against 180 countries, which he termed 'Liberation Day,' plunged the world's leading economy into a global trade conflict.

The last time we witnessed a tariff barrier of this scale was in the 1930s, under President Hoover, a move that precipitated a collapse in world trade and a U.S. depression. Small wonder, then, that Trump's tariff show has left financial markets, both the old guard and the new kids on the block, feeling shaken.

In a way, we were warned.

Tariff is the most beautiful word to me"

"Tariff is the most beautiful word to me" has become a tagline for Trump, and already during Trump's first presidential term (2017-2020), he tried to curb China's rise as a new superpower by starting a trade war against them. However, few anticipated that a second Trump term would unleash a multi-faceted trade war, disrupting international trade and the established world order.

The daily uncertainty surrounding Trump's actions has generated investor anxiety rivaled only by the 2008 financial crisis and the 2020 pandemic – the sole events since 2000 to induce greater market jitters than Trump.

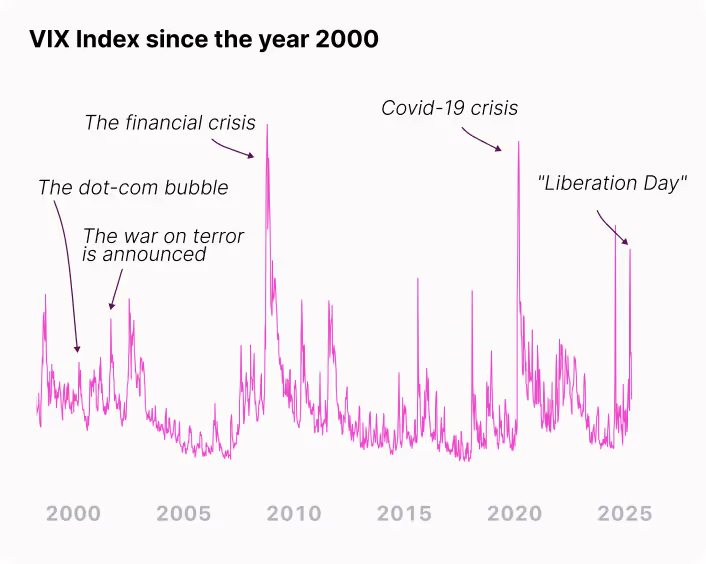

The Fear and Greed Index

We can track the market's nervousness using the VIX Index (Volatility Index), also known as the Fear and Greed Index. Basically, this index tells us how many ups and downs people expect in the American S&P 500, so it's a pretty good sign for the global stock market, too.

In periods of market stability, the VIX Index typically ranges between 10 and 20. During the 2008 financial crisis, the index peaked at 80.86 in late 2008, and during the COVID-19 pandemic, it reached a high of 82.60 in the spring of 2020.

On the Wednesday evening preceding President Trump's tariff announcement, the VIX closed at 21.51. Subsequently, the index increased, reaching 52.32 the following Tuesday. Notably, throughout April, the VIX registered intraday highs of approximately 80.

Tariff – or Not?

Each instance of President Trump's tariff implementation caused significant volatility in equity indices, and April, under his direction, became an exceptionally turbulent period for investors.

The following are the tariff announcements that corresponded with the most substantial stock market fluctuations:

- April 2nd: Trump introduces punitive tariffs aimed at 180 countries including 20% on goods from the EU and 34% on goods from China, on top of the existing 20% making it 54%.

- April 4th: The world's second-largest economy, China, retaliates against Trump with a 34% tariff on all imports from the US.

- April 9th: While the imposition of punitive tariffs was initially scheduled, Trump implemented a 90-day suspension for a select group of countries. However, the baseline 10% tariff on goods from all global nations, which took effect on April 7th, remains in place.

A few days earlier, Trump's advisor, Kevin Hassett, had been quoted as saying there would be a 90-day pause, but the White House quickly dismissed this.

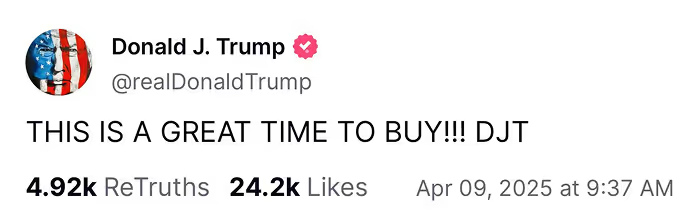

Four hours before Trump's own announcement of a tariff pause, he wrote this message on his own media platform, Truth Social: THIS IS A GREAT TIME TO BUY!!

On the same day, Nasdaq closed with an increase of more than 12%, the S&P 500 soared by 9.5%, and the Dow Jones rose by almost 8%. When the European markets opened on Thursday morning, investors were ready with their shopping bags, and we saw increases from the start of the day of up to 10%.

Later that day, however, Trump raised tariffs on Chinese goods from 104% to 125%, and on April 10th, he increased it to 145%, as the White House had forgotten to include tariffs on Fentanyl.

- April 11th: China raises its tariffs on the US from 84% to 125%.

- April 12th: Smartphones, computers, and microchips are exempt from Trump's tariffs.

- April 13th: Correction: Electronic goods will be subject to a separate tariff, with an effective date two months later. Concurrently, tariffs on pharmaceuticals are also announced.

- April 17th: Trump states that he may drop further tariff increases against China.

- April 22nd: At a private JP Morgan meeting, US Treasury Secretary Scott Bessent deemed the China tariff conflict unsustainable, citing no ongoing negotiations and a potential multi-year timeline. China, meanwhile, reports no contact with the US.

We're currently witnessing a standoff between the world's two dominant figures: Xi Jinping of China and Donald Trump of the United States.

I expect that Trump will likely concede first, given the immediate and significant impact on the American consumer and economy. While China faces its challenges, notably a struggling real estate sector, they have been strategically preparing for this type of scenario since the initial trade disputes with Trump.

Furthermore, it's crucial to acknowledge China's strategic advantage: control over critical raw materials essential for our green and sustainable future. China holds a leading position in the global rare earth market, both in mining and processing.

This reality is a key underlying factor in Trump's trade policies and his interest in Greenland, which possesses substantial raw material reserves.

Growing Distrust

However, it's not the large volatility and falls in stock prices that have prompted Trump to put part of his trade war on hold. It's the development in the bond market.

Historically, US government bonds have served as a traditional refuge for investors when the stock market faces a storm. However, Trump's tariff policies have disrupted this established correlation, altering the financial system's typical risk-aversion response.

To understand what's happening, we need to briefly touch on the US household budget.

The US. Household Budget

The US national debt has ballooned to approximately $36 trillion, creating a significant fiscal challenge.

To manage this debt, the US issues long-term government bonds that eventually require repayment.

Decades of overspending and persistent budget deficits have forced the US government to continuously issue more bonds to finance the shortfall. This year alone, the US must borrow $9 trillion simply to cover maturing bonds.

Therefore, Trump had to partially hit the brakes when the interest rate on a 30-year US government bond was at one point higher than the interest rate on a 30-year Greek government bond.

This means that investors would rather lend money to the Greek state than the American one (!)

A fundamental distrust has emerged among investors regarding the U.S. economy, fueling discussions about the dollar's role as the global reserve currency.

Trump Wants Interest Rate Reductions

Adding to this, President Trump has publicly criticized the Federal Reserve, labeling Chairman Jerome Powell a 'major loser' and expressing his desire to remove him from office.

Trump's objective is to expedite interest rate reductions to mitigate the economic impact of tariffs and trade barriers.

However, in contrast to the European Central Bank, which implemented its seventh consecutive rate cut in April, Powell and the Federal Reserve remain focused on combating inflation, a process that typically requires raising interest rates.

The U.S. President's interference in the central bank's operations poses a threat to the FED's independence.

This independence is the cornerstone of investor confidence and the reason why foreign investors hold trillions of dollars in U.S. Treasury bonds. While President Trump has since stepped back from directly threatening Powell's dismissal, he continues to vocally advocate for lower interest rates.

The Power of Consumers

Uncertainty surrounding the U.S. economy has significantly increased under President Trump's policies, reigniting concerns about a potential recession in the U.S.

In April, the International Monetary Fund (IMF) released its semi-annual growth forecast, downgrading U.S. growth by 0.9 percentage points to 1.8% for 2025 – a full percentage point decrease from the 2.8% growth recorded in 2024.

A trade war has a contagion effect on global growth. The IMF's projection for overall global growth in 2025 stands at 2.8%, a 0.5 percentage point downward revision from their previous forecast in October last year.

Eurozone countries experienced a smaller downward adjustment of 0.2 percentage points. However, the EU is already facing weak growth, with particular anticipation for Germany's new government to accelerate its investment program. Growth forecasts for the U.K. and China were also revised downwards by 0.5 and 0.6 percentage points, respectively.

Consumer Confidence: The Tipping Point of Recession

Consumers play a critical role in a recession (in the U.S., private consumption accounts for 70% of GDP).

Rising prices (inflation) and uncertainty about the economic outlook lead to reduced consumer spending. This, in turn, causes a decrease in demand for businesses' goods and services.

Here's what Scott Boatwright, CEO of Chipotle Mexican Grill, stated following the company's Q1 2025 earnings report on April 23rd:

'Saving money because of concerns around the economy was the overwhelming reason consumers were reducing the frequency of restaurant visits.'

Robert Jordan, CEO of American Airlines, commented on the largest decline in U.S. domestic flights outside of the pandemic period:

I don’t care if you call it a recession or not, in this industry that’s a recession

U.S. consumer confidence has been steadily declining, falling for the fourth consecutive month in April. We have to go back to 2022 (the end of the pandemic) to see similar levels of pessimism among American consumers.

In Europe, consumer sentiment is as negative as it was during the financial crisis. This does not bode well for a crucial driver of economic growth, and it is historically significant that one individual – the U.S. President – can generate such substantial uncertainty about the future.

A Critical Earnings Season

The upcoming earnings season, which gained momentum after Easter and extends through the end of May, will reveal the performance of companies during the first quarter of 2025. Analysts have already significantly lowered their earnings expectations for the first quarter, from 11% at the start of the year to just 6% currently.

However, the most crucial information will be the outlook provided by companies regarding future earnings. What are their projections in an environment characterized by increased costs, supply chain disruptions, rising inflation due to tariff barriers, and cautious consumers with a pessimistic view of the future?

Furthermore, will investors continue to shift capital from the U.S. to Europe, where the European STOXX 600 index has maintained a positive year-to-date return of approximately 3%, in contrast to the S&P 500's nearly 6% year-to-date decline?

More turbulence is undoubtedly on the horizon, and the true impact of President Trump's first 100 days in the White House will become clearer over the next few months.