6/10/25

From London to Paris to Wall Street – Tech and Gold Shine in an Autumn of Rates and Politics

In the US, the central bank’s rate meeting raised questions about global financial stability.

September closed on a note of political and economic turbulence to both the UK and France.

In the US, the central bank’s rate meeting raised questions about global financial stability, while “hybrid warfare” has emerged as the buzzword in this month’s geopolitical debate.

Meanwhile, in the markets, gold and US tech stocks set new records. In contrast, European equities had a quieter late summer and lost further momentum in September.

Looking at investors’ “temperature meter” – the Volatility Index – it remained close to a resting state. Throughout the month, the index stayed below 20%.

A Crucial Autumn for Europe’s Second-Largest Economy

We begin with a trip to London, where the US president has been on a three-day state visit. Unlike his first visit, the British royal family and politicians were front and center this time, dressed in their finest attire.

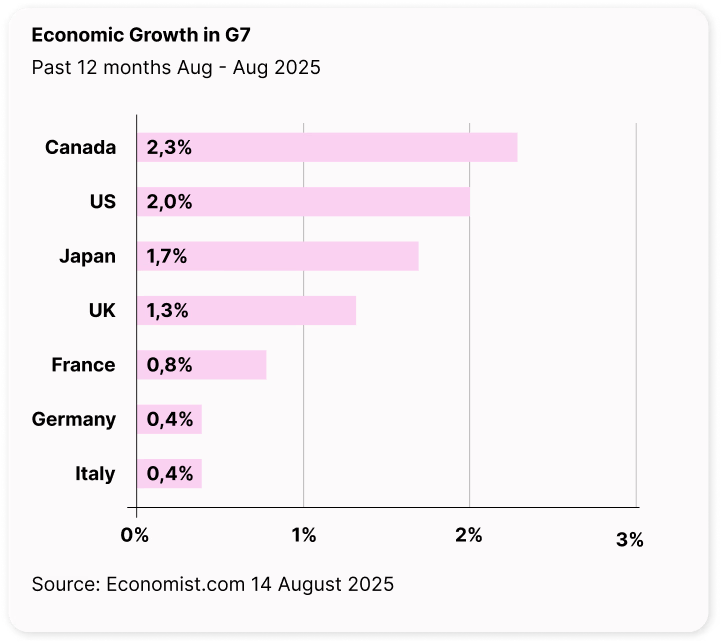

Why this shift in approach from the British government? The UK economy in autumn 2025 finds itself caught between political promises and economic realities. After a strong start to the year, with the fastest growth among G7 nations, the outlook has now become more subdued.

The International Monetary Fund and the Office for Budget Responsibility – which monitors the government’s budget plans and outcomes – both now forecast growth of around 1–1.2% in 2025. This is far below the Labour government’s ambitions to create a more dynamic economic climate.

At the same time, US tariffs on British goods continue to weigh on exports, while inflation remains well above the Bank of England’s target, even after five rate cuts over the past year.

For UK Finance Minister Rachel Reeves, the situation is a political balancing act. She has pledged to ensure growth and responsible fiscal policy without increasing debt. But with rising inflation and unemployment, and a growing trade deficit, the pressure is mounting ahead of the autumn budget on November 26.

The finance minister herself has described the UK economy as “stocked.” This is reflected in the yield on 30-year British government bonds, which reached their highest level since 1998 at the start of the month – investors are clearly pricing in high risk when buying UK government debt.

Europe’s Silicon Valley?

The UK Labour government is under pressure – not only economically, but also politically from the right, as seen across Europe.

Trump was therefore seen as an opportunity to give Prime Minister Keir Starmer a boost, in the form of US investments and a potential easing of tariffs on British exports to the US.

However, the existing trade agreement was not improved. Instead, a new technology pact – the “Tech Prosperity Deal” – was signed. According to Starmer, the deal has “the power to change lives,” with “billions now set to flow both ways across the Atlantic.”

The agreement aims to position the UK as a hub for AI and data infrastructure, with US companies committing £31 billion ($42 billion) in investments across cloud, semiconductors, and nuclear research:

- Microsoft is investing £22 billion in the UK’s largest AI supercomputer.

- Nvidia is deploying 120,000 GPUs in the UK – the largest rollout in Europe.

- Google is investing £5 billion in a UK data center and DeepMind research.

With a GDP that ranks the UK as Europe’s second-largest economy, after Germany and ahead of France, these new investments are not only a welcome boost for Keir Starmer but also send a positive signal for the rest of Europe.

Many in the UK tech industry see the investments as clear recognition of the country’s potential as a tech nation. Skeptics, however, question who will actually benefit and whether the UK can maintain its technological and regulatory independence.

France – the EU’s Problem Child

We move from London to France. The political drama in Paris has made international headlines throughout September. After a bitter clash over taxes and public spending aimed at reducing the country’s large budget deficit, Prime Minister François Bayrou was ousted in a vote of no confidence.

President Macron has since handed the baton to Sébastien Lecornu – Macron’s seventh ministerial appointment as president and the fourth since the start of 2024.

Lecornu now faces the unenviable task of assembling a fragile coalition and restoring confidence in the country’s economic direction. The challenge is monumental, with public debt having crept up to around 115% of GDP.

Credit rating agency Fitch also downgraded France’s credit rating from AA to A+ in September (AAA being the highest rating).

This sends a signal to markets that patience with Paris is running thin. At the same time, it becomes more expensive for the French state to sell debt through government bonds (a scenario familiar from both the UK and the US).

While Southern European countries are currently praised for fiscal discipline – Spain and Portugal both saw their credit ratings upgraded – France still stands out as the eurozone’s problem child.

This underscores Europe’s pressing need for Germany to accelerate its new strategy, focusing on major investments in defense, infrastructure, and climate initiatives.

US Interest Rate Cut

This month’s key event was the Federal Reserve’s interest rate meeting.

For the first time in 2025, the central bank cut the benchmark rate by 25 basis points to a range of 4.00–4.25%, while signaling two more cuts later in 2025 and one in 2026.

The rate cut follows weaker-than-expected job data over the summer and sends a signal to the market that the Fed is prioritizing a softer labor market over rising inflation.

Ahead of the meeting, the US president attempted to remove Fed Governor Lisa Cook while simultaneously placing his close economic advisor, Stephen Miran, on the board.

Unsurprisingly, Miran was the only member to vote for a double rate cut of 50 basis points.

The episode has intensified investors’ concerns over the Fed’s independence. Fed Chair Jerome Powell repeatedly emphasized that the central bank operates free from political pressure, yet the Fed’s projections now closely align with the president’s preferences.

The Fed’s independence is crucial for the US dollar. When the central bank makes decisions free from political influence, it strengthens confidence in the dollar as the world’s primary reserve and trade currency, as well as a “safe haven” in uncertain times.

A loss of independence could weaken the dollar, increase market volatility, and threaten stability across the global financial system.

Gold – the Safest Haven?

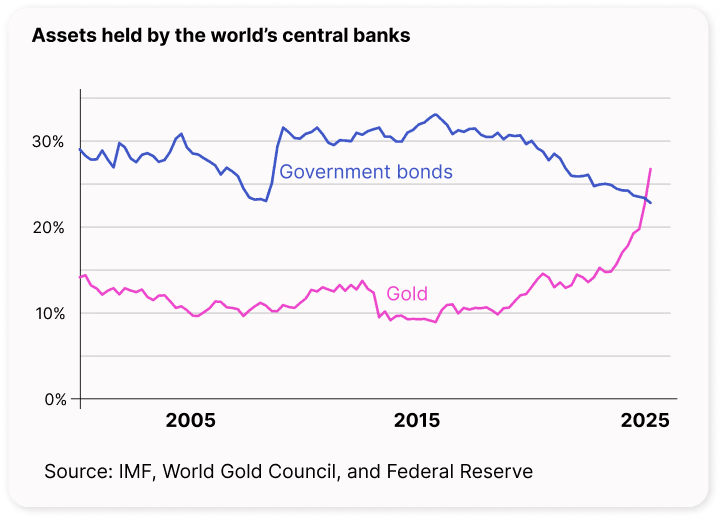

While traditionally safe havens such as the US dollar and government bonds are under pressure, gold continues to hit record levels. This year, the precious metal has risen by just over 40%.

The surge in gold prices accelerated in the wake of the war in Ukraine, driven primarily by central bank purchases and strong demand from Asia, particularly China and India. As a result, for the first time since the 1990s, central banks now hold more gold than US government bonds in their reserves.

Concerns over political and economic developments in the US have also pushed gold prices higher, as has the situation in France and the UK.

Throughout September, we have seen repeated violations of European airspace. This includes drones over airports in Denmark and Norway, incursions into Polish airspace, and incidents in Lithuania and Romania, as well as cyberattacks on airports across Europe – now being described as part of a hybrid threat.

All of these developments suggest that Putin is testing NATO’s cohesion. This uncertainty is pushing investors further toward gold, with Western investors increasingly adding gold ETFs to their portfolios.

Tech and Trade Take Center Stage

September brought a lot to the table, so it may be surprising that we didn’t see bigger swings in the VIX index. Credit goes to US tech companies.

While most European equity indices closed September in the red, the AI investment story continues to push US indices to new highs. Several key developments hit the market in September:

- World-leading chipmaker Nvidia announced a strategic partnership with OpenAI, the company behind ChatGPT. Nvidia plans to invest up to $100 billion in OpenAI to build new data centers and infrastructure, which Nvidia CEO Jensen Huang calls the largest AI infrastructure project ever.

- Nvidia is also investing $5 billion in Intel. Together, the two companies will develop microchips for computers and data centers. Intel recently received funding from the US government, and rumors are circulating that Apple may soon join the initiative.

- The biggest surprise came in a new partnership between Nvidia and Alibaba, one of China’s largest e-commerce and cloud companies. The two firms will collaborate on global data centers and the development of AI products.

We are thus entering an exciting final quarter of 2025, with earnings season kicking off in October. The key question remains whether tech stocks can meet investors’ earnings expectations and continue to drive US indices to new record highs.

And no, I haven’t forgotten about trade and tariff agreements. Investors have been encouraged by the steady progress of negotiations between China and the US, including phone calls between the two presidents.

However, Xi and Trump face a deadline in early November.

In October, attention on tariffs is expected to rise again, including in specific sectors such as the pharmaceutical industry.