2/9/25

How a Kayaking ‘Aha’ Moment Sparked a £2,500-a-Month Property Side Hustle

Suddenly it hit me: I could actually make money while doing something entirely different - like kayaking.

Back in 2021, I had a life-changing aha moment. I was paddling a kayak through the Greek islands when it suddenly hit me: I could actually make money while doing something entirely different - like kayaking.

Out there on the water, with the sun on my face, I pulled out my phone and bought some shares of Royal Unibrew - a stock I’d had my eye on for a while.

That was when I truly understood: by investing, my money could be working for me while I was free to do what I loved - paddling, sipping wine, or hiking in the mountains.

And in the long run, that could mean real returns (or so I hope - because I still own those shares today).

For me, investing isn’t just about having more to spend. It represents something deeper: freedom.

And that moment on the kayak was the spark that led me to real estate investing, two vacation homes, and an extra £2,500 a month in income.

Here’s how I got there.

Where the Idea Began

I’ve always been fascinated by money. Not because I love spending it or buying expensive things, but because I value the opportunities money can create. More than anything, I never want to feel limited by what I don’t have.

So I’ve always been curious about how to earn more. The obvious way was through work.

But there’s only so much time you can trade for money - so I started exploring other income streams.

My first step was investing in stocks, and I was quickly hooked. Through investing, I realized it was possible to make money while pursuing other interests. The thrill of earning money while fully living in the moment was addictive.

At the time, I dreamed of living off stock market returns. And naturally, when you love investing, you want more capital to invest - because the more you invest, the more you can earn.

From Stocks to Bricks and Mortar

That’s when I started looking for ways to build cash flow - money I could reinvest.

Real estate seemed perfect: tangible assets, consistent income, a positive market outlook, and low interest rates.

The catch? It’s expensive. You needed a hefty savings buffer and a solid income to convince a bank to lend.

In 2023, my partner and I were still students, living on student loans - not exactly banker-approved. At the time, I assumed the only way to profit in property was to buy an apartment in Copenhagen (where I live). With those prices, that was out of reach for us.

We began researching alternatives - REITs, property funds, other indirect routes - but they felt too abstract.

The Lightbulb Moment: Short-Term Rentals

Everything changed when we rented out our own apartment on Airbnb.

My partner and I crunched the numbers one night: renting our flat for just seven nights a month would cover our entire housing costs.

The problem? We needed the flat ourselves most of the time.

But we saw the potential in short-term rentals, and realized you could earn more this way than through traditional long-term leases. So we looked into buying an apartment purely to rent it on Airbnb.

That’s when we hit another roadblock: Danish law requires you to live in year-round properties, and you can only short-term rent them for up to 70 days a year. On top of that, we still couldn’t afford a Copenhagen apartment.

Then came the game-changer: you can legally buy a vacation home (with no primary residence requirements) and rent it out almost as much as you like. Vacation homes are also much more affordable than city apartments.

Our First Vacation Home

My partner Benjamin and I talked about it endlessly. We researched, debated, and researched some more. On a trip in September, we finally decided to stop dreaming and start doing.

We spent the rest of the vacation on the internet searching for vacation homes for sale and mapped out a concrete plan to buy one as students.

We booked a bank meeting and started viewing properties. Our budget was up to 1.5 million DKK (~£170,000).

That might sound surprising for two students, but there were a few key reasons it was possible.

Education is free in Denmark, and most students don’t have big debts - in fact, we get paid a small amount to study. That meant I was able to save up while still in school.

On top of that, we’d both been investing in stocks for a few years and had part-time jobs, which helped us qualify for a mortgage.

We focused on an area we knew well, where there was a good selection of affordable vacation homes. After a few months, we found “the one.” Unfortunately, another couple outbid us by just 5,000 DKK (~£570). Ouch.

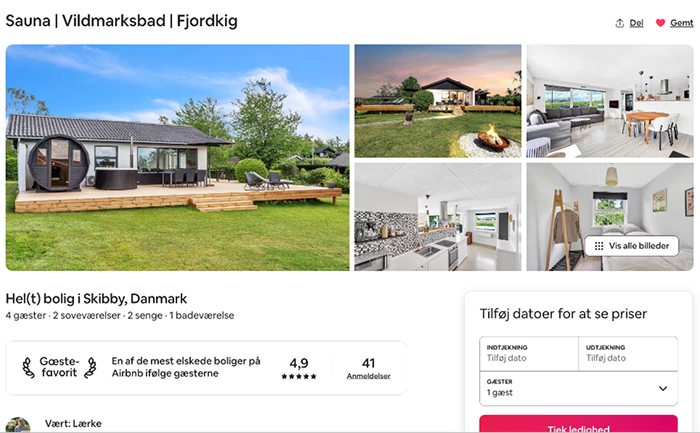

We kept searching. Finally, on March 8, 2024, we signed the contract for our first vacation home: 74 square meters, 1.3 million DKK (~£150,000), two bedrooms, an older bathroom, and an open-plan kitchen/living space.

Originally, we planned a big renovation. But in the end, we built a large wooden deck, added a sauna and hot tub - and suddenly, our little vacation home had a big competitive edge.

From Zero to Fully Booked

We got the keys to the vacation home in April 2024 and spent the next 2–3 months getting it ready to list on Airbnb. We decorated the house, built the large wooden deck, and had professional photos taken so we could show the place at its best. Once everything was ready, we uploaded the listing to Airbnb in early July 2024.

Within just a few hours, our very first booking came in: a family from England wanted to stay. And not in a few weeks - they wanted to arrive the very next day!

We definitely hadn’t expected that. We quickly packed up and drove out from Copenhagen to prepare the house. We deep cleaned the entire place, washed all the bed linens and towels, set up the key box, and filled the hot tub with fresh water.

We managed to get everything done just in time - and the next day, our very first guests arrived. They paid 2,500 DKK (~£285) for three nights.

After that, the bookings kept pouring in. The rest of July was almost fully booked in no time, and August quickly followed - we didn’t have a single free day left in our Airbnb calendar.

Already in our first month of renting, we earned enough to cover all of our expenses - and more. It exceeded all expectations!

The Numbers

Aside from having a great getaway spot ourselves (our tiny Copenhagen apartment does get cramped), this was always meant to be a money-making project.

So here is the math on how much we actually have as extra income after expenses:

We bought our first home for ~£150,000, putting 25% down. We took a mortgage for the rest. Our monthly costs are around £1,150 - including mortgage, utilities, wood for the hot tub, and cleaning.

We generate about £2,500 per month on average - netting us roughly £1,350 profit each month.

Money and Relationships

I’ve learned so much from this process. And first and foremost: if you go into property investment with your partner… be prepared to talk about money. Often.

That applies to the fun conversations - things like:

- “What should we use the money we’re earning for?”

- “How can we optimise this?”

- “What are our dreams?”

But it’s equally important to have the more difficult conversations:

- “What if this doesn’t go the way we hope?”

- “What if we break up at some point?”

My best advice: make sure you discuss everything - both the fun and the tough stuff. One thing is certain: it’s much easier to talk about hard topics while you’re still good friends. So get those conversations out of the way early, even if you obviously hope you’ll never need them.

And here’s an extra bonus: couples who regularly talk about money tend to be happier!

A study shows that 78% of couples who talk about finances frequently say they’re happy in their relationship, compared to just 50% of couples who rarely discuss money.

Many people find talking about money with their partner boring - or even uncomfortable. Personally, I don’t. Quite the opposite!

Some of the best and most fun conversations I have with my partner are about our dreams and future plans - including the financial aspects.

And since buying our second vacation home, those financial conversations have only grown.

The Second Vacation Home

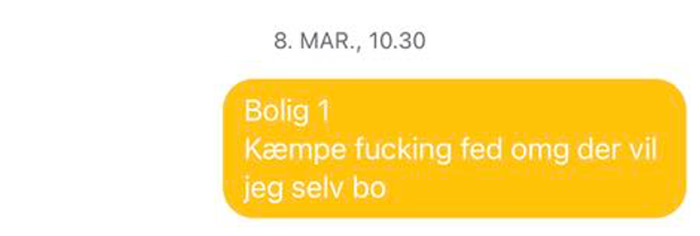

Exactly one year after our first purchase, we drove to Falster (A small island in Denmark) to view vacation homes in Marielyst. We had 10 properties on our list.

We Fell Head Over Heels - and Blew the Budget

On March 8th - exactly one year after signing for our first vacation home - we headed to Falster to view potential properties in the seaside town of Marielyst. We had a packed schedule ahead: ten vacation homes on our list.

We had decided that for our next purchase, we wanted a large home with room for lots of guests. Partly because we both come from big families, and partly because the more people a house can accommodate, the higher its potential rental income (though of course, many other factors also come into play).

With that in mind, we had also increased our budget. Both of us had transitioned from students to full-time employees, so the bank was now a little more cooperative. We set a maximum budget of 3.2 million DKK (~£365,000), though naturally, we hoped to find something for less.

Still - there was one particular house that completely stood out from the rest: sea view, pool, spa, and loads of space. The only problem? It was listed at 3.6 million DKK (~£410,000). Well above our limit. But since we were making the trip anyway, we figured we might as well go see it - if only for inspiration.

To help keep track of the many viewings, we had agreed to write a few notes after each one, so we’d remember our first impressions by the end of the day.

The first house on the list was the expensive one.

After the tour, I opened my phone and wrote:

“House 1: absolutely amazing. OMG, I want to live here.”

And that was it.

I didn’t write a single note about any of the other homes we viewed that day - they simply couldn’t compare. We knew there was no way around it - we had to call the bank and find out if there was any way to stretch our budget a little further.

Thankfully, after some discussion, the bank approved us to borrow up to 3.5 million DKK (~£400,000).

Next, we had to convince the sellers to come down on price. After a bit of back and forth, they finally agreed to sell at exactly that amount. A few weeks later, both parties had signed the purchase agreement.

The Flip Side

Even though we find this vacation home project exciting and fun, the biggest driver for us has always been improving our personal finances in the long term. And that means accepting certain short-term sacrifices.

One of the main trade-offs is that right now, we have limited ability to buy a home for ourselves - a permanent residence we could live in.

We absolutely dream of owning our own house one day. But with two mortgages on vacation properties, it’s going to be difficult to convince the bank to lend us more for a third property.

So we’ve made a conscious choice: to postpone our own homeownership dream for now, and prioritise vacation home investments to build an additional income stream alongside our regular salaries. This way, we’re improving our long-term financial position.

At the same time, it’s important to be clear: investing in vacation homes for rental income is far from passive.

On the contrary, it takes ongoing time and effort - communicating with guests, cleaning, maintenance, and quick troubleshooting when things break.

Of course, you can choose to work with a property management company to handle some of these tasks, but that comes at a cost. Most agencies charge between 20% and 40% of your rental income, which naturally cuts into your return significantly.

For us, it made more sense to manage everything ourselves to keep more of the earnings, and maintain full control over the guest experience.

What’s Next?

It’s wild to think that just a few years ago, my partner and I chose to pursue this dream. Today, we own two vacation homes, have a stable side income, and feel empowered by working smarter, not harder.

It’s taken courage, patience, and a lot of research - but most of all, we acted.

For us, these homes aren’t just “investments in bricks and mortar” - they’re investments in our future, our relationship, and our dreams.

If you’ve ever dreamed of investing - whether in stocks, real estate, or something else - I hope my story gives you the push to start.

Freedom rarely falls into your lap. You have to seek it, plan it, and build it.

Sources:

- https://www.forbes.com/sites/reneemorad/2016/10/31/frequent-money-talks-could-lead-to-a-happier-marriage-study-suggests