2/9/25

Tariffs, Debt, and Big Tech Define May's Markets

May was a rollercoaster ride! One thing is for sure: we can always count on the U.S president to stir things up

Trump's TACO tactics and U.S. debt stirred up market unpredictability this past month.

Investors also grappled with earnings from the world's biggest companies, and then, just before month-end, a tariff bombshell hit the White House.

Rollercoaster month

May began with high spirits in the financial markets.

Alongside increasing daylight hours, the world's most important stock index, the S&P 500, crept higher than it was before "Liberation Day" on April 2nd when Trump launched the U.S. into a global trade war.

The positive sentiment grew as earnings reports, especially from major U.S. tech companies, rolled in. Simultaneously, we observed a more positive tone in the trade and tariff conflict, particularly between the U.S. and China.

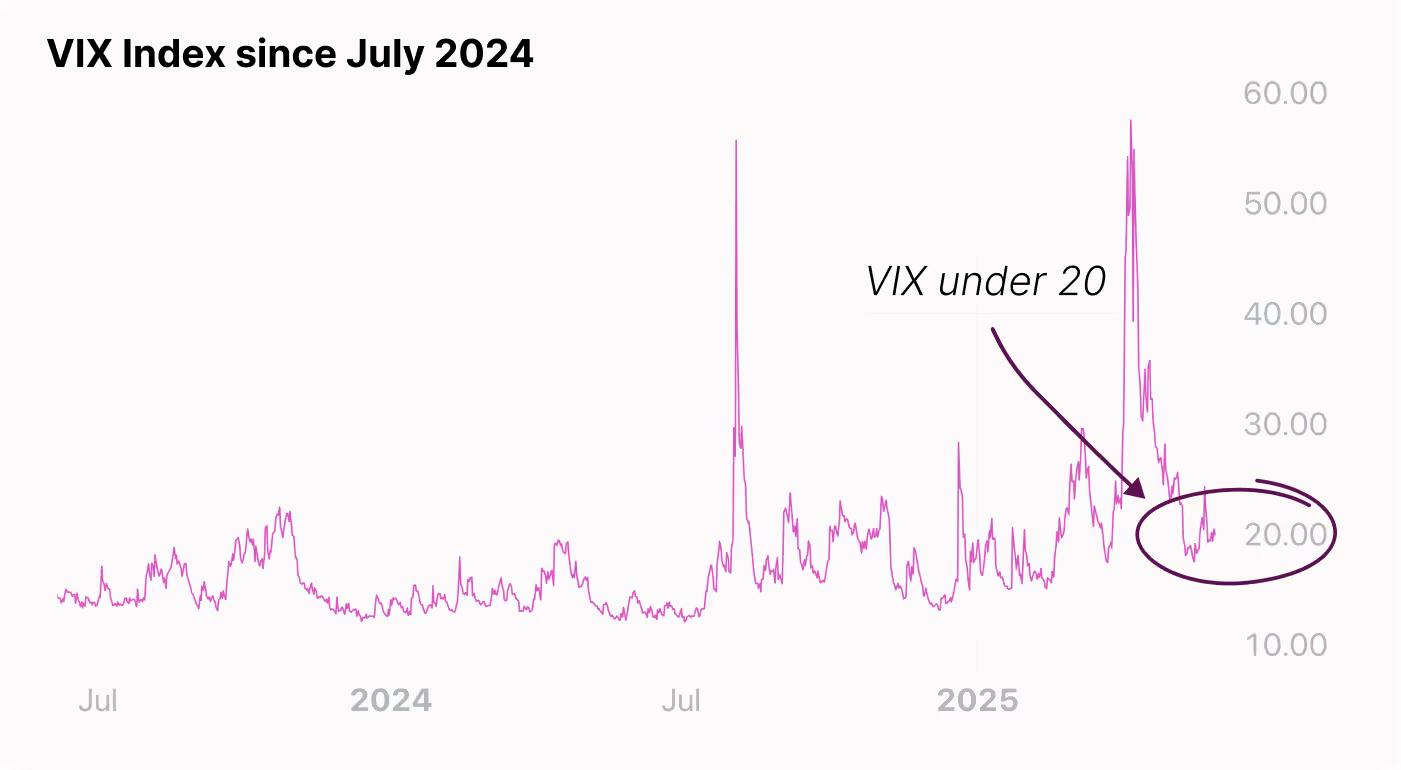

The VIX index, which measures market volatility, dipped below 20 during the month for the first time since March this year. This indicated that investors' nerves had somewhat settled after April's significant fluctuations, which saw market anxiety levels approaching those experienced during the pandemic and the financial crisis.

However, we can always count on the U.S. president to stir things up.

Over the month, grey clouds gathered over the market in the form of renewed concerns about America's growing debt.

It also became clear that Trump has difficulty keeping his hands off the tariff trigger.

Trump's tactics in trade negotiations have paved the way for a completely new trading pattern in the market, which a Financial Times columnist has dubbed "TACO Trade" – Trump Always Chickens Out.

This pattern, in short, involves Trump first making a wild declaration, similar to "Liberation Day" on April 2nd, which he then quickly retracts.

This initially sparks fear in the market and leads to a sell-off of stocks, followed by an immense sigh of relief and a stock rally once the U.S. president pulls back his extreme statements.

A Chinese and European "TACO"

Mid-month, during a weekend meeting in Geneva, Switzerland, between the U.S. and China, the world's two largest economies brokered a 90-day truce in the tariff war, significantly reducing the duties dramatically imposed in April.

This agreement temporarily saw the U.S. lower its tariffs on Chinese goods from 145% to 30%, while China reduced its tariffs on American goods from 125% to 10%.

Within just one month, we transitioned from a frontal trade war to an almost complete withdrawal.

The pace of the agreement suggests both parties, while rhetorically strong, stand on an uncertain economic foundation.

The deal certainly doesn't resolve the deeper disagreements between Washington and Beijing.

Still, but the de-escalation of the U.S.-China trade conflict sent the global stock market rising, and fears of a global recession subsided.

Temporary calm had settled on one trade front, but just 14 days later, the American president turned his attention to the EU.

On his social media platform, Truth Social, Trump threatened the EU with a 50% tariff starting June 1st, causing both European and American stocks to fall.

However, during the subsequent weekend, Trump had a phone conversation with EU Commission President Ursula von der Leyen.

Early Monday morning, he announced in a post that the U.S. and the EU had agreed to a tariff pause until July 9th.

While the U.S. and EU remain far apart in negotiations, this announcement brought renewed optimism to the stock market.

Then, at the very end of the month (May 28th), a bombshell landed in the White House. The U.S. Court of International Trade, which had remained silent until now, overturned the president's tariffs, citing that Trump had exceeded his constitutional authority.

This effectively pulled the rug out from under the entire foundation of Trump’s "Liberation Day" tariff project!

However, the jubilation across various newspaper front pages lasted less than 24 hours. It was then announced that an appellate court in the U.S. had reinstated the president's tariffs while an appeal was being processed.

Life in the markets is indeed a rollercoaster!

U.S. Economy Weakens Global Outlook

A looming global trade war isn't the only concern on the financial markets' radar.

Growing anxieties about the stability of the world's largest economy added fuel to the fire this month when ratings agency Moody's downgraded the U.S. credit rating from its top-tier AAA to the second-highest rating, AA1.

All countries are assigned an economic rating, which impacts their ability to borrow money. The highest rating, AAA, is currently held by countries like Denmark, Switzerland, Germany, and Canada.

With this downgrade, Moody's aligns with the other major rating agencies: Standard & Poor's removed its top rating in 2011, and Fitch followed suit in August 2023. (For insight into the role of credit rating agencies, I highly recommend the film "The Big Short" about the 2008 financial crisis).

The U.S. downgrade stems from the country's growing debt and persistently increasing overspending, leading to government budget deficits. The U.S. has run household budget deficits for many years, but now the trade war and Trump's new, large legislative package have made financial markets even more nervous.

Trump himself dubbed his proposed legislation "The big, beautiful bill." It includes significant tax cuts that will further increase the national debt.

The package narrowly passed the House of Representatives in May with 215 votes for and 214 against and is now set for a decision in the Senate, likely at the beginning of June.

Late in the month, the U.S. needed to borrow money again, and an auction for 20-year U.S. Treasury bonds saw unusually low demand. Investors are simply reluctant to finance American overconsumption, which simultaneously underscores the declining confidence in the U.S. as a solid economy and safe haven for investors.

Jamie Dimon, CEO of major investment bank JP Morgan, warned that equity markets are overly optimistic and not realistically addressing strained U.S. public finances, increased tariffs, and geopolitical tensions.

According to Dimon, current stock prices do not reflect the risk of higher inflation and, in the worst-case scenario, stagflation – a combination of rising prices and falling growth.

Several key economic indicators and confidence indexes also point towards a weaker U.S. economy.

For instance, the U.S. experienced negative growth in the first quarter of 2025 for the first time in three years.

Maurice Obstfeld, former Chief Economist at the International Monetary Fund and economic advisor to President Obama, stated in an interview with the Danish newspaper Børsen that we will soon see a significant weakening of the U.S. economy in key figures.

Will the AI Growth Narrative Hold?

Despite the prevailing economic and geopolitical uncertainties, the market found comfort in a raft of strong first-quarter earnings reports.

These results indicated that global companies stand on solid ground and aren't immediately being derailed by Trump's policies.

Naturally, the spotlight shone brightest on U.S. Big Tech and the world's most valuable companies. Microsoft, Alphabet, and Meta all delivered robust earnings, showcasing significant growth, particularly in AI and cloud services. This initially reassured investors that the AI-driven growth trajectory appears sustainable.

Chip giant Nvidia also reported surprisingly strong figures, fueled by robust demand for its AI chips. CEO Jensen Huang underscored Nvidia's pivotal role at the heart of the ongoing AI revolution, emphasizing how fundamental artificial intelligence has become to our society.

However, the ongoing trade conflict between China and the U.S. is impacting Nvidia.

The company anticipates an eight-billion USD loss due to the restrictions the Trump administration has placed on its advanced H20 chips, which were specifically tailored for the Chinese market.

Jensen Huang noted that limiting Nvidia's products won't halt China's AI development; instead, it will accelerate China's domestic innovation, inadvertently strengthening competitors like Huawei.

A key question leading into the next earnings report will be whether Nvidia can circumvent these restrictions and maintain its position in the Chinese market.

Earnings from Amazon and Apple were less positive, as both companies are more susceptible to shifts in consumer demand and disruptions in global supply chains than fx Meta and Microsoft.

The same applies to Tesla, though investors are focusing on signs that Elon Musk may be tiring of Trump and is therefore returning to his CEO responsibilities. His presence has been keenly missed; while he's been preoccupied with DOGE-related projects, Chinese automaker BYD has, for the first time, sold more cars in Europe than Tesla.

Overall, over 70% of S&P 500 companies reported better-than-expected earnings. Unsurprisingly, the word "tariff" increasingly crept into companies' forward-looking statements. According to a report from IoT Analytics, 43% of publicly traded companies mentioned "tariff" in their Q1 2025 earnings calls, a 190% increase compared to Q4 2024.

Retail giant Walmart—the world's largest private company by revenue and employee count—stated it would pass the 30% tariffs on Chinese goods onto its prices.

This would lead to significant price increases on many essential American supermarket purchases, fueling inflation. Trump subsequently urged Walmart to "Eat the tariffs," but given the already thin retail margins, Walmart will likely have to raise prices to preserve its bottom line.

Sell the U.S. Narrative Gains Traction

In Europe, companies generally delivered a solid first quarter, with the defense and arms industry maintaining its momentum.

Germany's DAX index, which has climbed nearly 20% year-to-date, closed May with a gain of approximately 6%. The UK's FTSE100 ended the month up almost 3%, and in Denmark, the C25 posted a gain of nearly 7%—though it remains down slightly over 2% for the year.

The prevailing market narrative continues to be that capital is flowing out of the U.S. and into Europe and Asia. While the S&P 500 closed the month up just over 6%, it is only barely in positive territory for the year.

In contrast, the tech-heavy Nasdaq index saw a more robust gain of over 9% for the month and 7% year-to-date. Notably, the top-performing tech stocks so far in 2025 have been Chinese, with "The Terrific 10" (the ten major Chinese tech companies including Alibaba, BYD, Meituan, (Meiduan) Tencent, and Xiaomi (Shaw-me)) outperforming the U.S.'s "Magnificent 7" in terms of returns.

As earnings season wraps up, market participants will redirect their full attention to key macroeconomic indicators and evolving interest rate trends.

The judicial overturning of Trump's retaliatory tariffs means companies and investors enter June with renewed uncertainty regarding market frameworks and direction.

The best advice remains: breathe deeply and avoid panic selling.

Review your portfolio, evaluate what your companies have communicated regarding their full-year expectations in their first-quarter reports—for instance, has a downgrade in expectations significantly altered the investment case? -and focus on long-term strategies and diversification.