.avif)

11/12/25

What I Spent This Week as a Biologist Making £60k

Ever wondered how others really manage their money?

Ever wondered how others really manage their money?

In the A Week in My Wallet series, we share it all, because talking about money shouldn't be off-limits.

Every week, an anonymous member shares a week of their spending: no names, no filters, just honest stories about life's everyday financial choices.

Ready to join the conversation and help make money talk less taboo? Share your own story via our form here.

Monthly Take-Home Pay (after tax): £3,100

Household Income: I live alone

Do you share expenses with someone? No

Dependents: One puppy

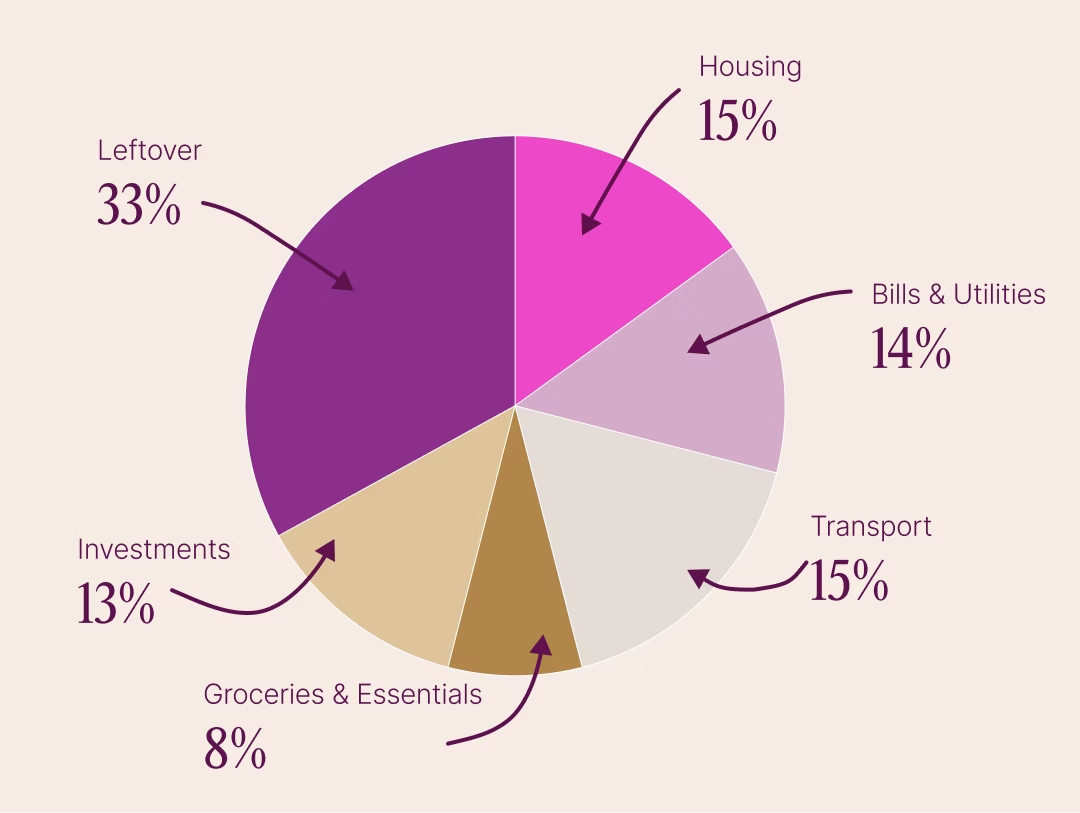

Monthly Budget Overview:

- Housing (loan payment): approx. £475

- Bills, subscriptions & utilities: approx. £427

- Transport (incl. leasing & insurance): £538

- Groceries & essentials: approx. £257

- Investments: approx. £398

My budget isn’t categorized according to the 50/30/20 rule, but I use it as a guideline to evaluate spending and prioritizing. For example, I chose to lease a car, so the extra costs under “transport” are included under the 30% for wants. I also use it to calculate what to allocate to savings/investments.

I use the Female Invest Excel budget sheet, where I’ve added tabs to see the breakdown of my spending.

Amount left each month after essentials (to spend, save or invest):

Approx. £560 for hobbies, takeaway, small maintenance and savings. There is a fixed transfer of approx. £870 directly to my savings to limit spending.

Dependents (if any):

Got a puppy this week, which means I’ll need to make some changes and re prioritise my budget going forward.

My Relationship with Money

Growing up, did your parents or guardians educate you around money?

It happened more indirectly. I saw my dad review receipts at the end of each month and put everything into an Excel sheet. My mom was good at finding things in thrift stores to save money.

So I’ve always been aware that you need to keep track of your spending. When I turned 18, I asked my dad for help to understand bills and how to pay them.

They also secured a savings account for me, which I didn’t know about until I wanted my driver’s license. I let them manage it until my mid-20s, which meant I had to ask for money transfers — making me think twice before spending. It gave me a financial safety net when I was young.

This has shaped how I view my finances and why I always want to have a buffer.

What was your first job and why did you get it?

I wanted a mobile phone, so I got a job delivering leaflets when I was 13. It was in the countryside with long distances between houses and so many leaflets that I couldn’t fit them in a bike trailer. My parents helped me.

Did You Worry About Money Growing Up?

No. I knew I couldn’t have everything I wanted, but I never felt we lacked anything. My parents were good at saving and prioritising.

At what age did you become financially responsible for yourself and do you have a financial safety net?

When I started high school at 17, I moved to a boarding school. When I turned 18 and received student grants, I paid for living there myself. My parents gave me about £60 a month as a supplement.

I’ve been fully independent since starting university. But I also had savings for my deposit and other expenses.

Do you worry about money now?

I’ve always been worried I couldn’t manage my finances and would overspend. That’s made me very cautious. It’s still in me, even though I’ve always managed fine and never lived beyond my means.

So I don’t worry about checking my bank account — only about big changes (like buying a house) that affect my general spending. I also have to remind myself that I am allowed to spend money on non-essentials. I’m getting better at it.

What is your biggest money regret?

Mostly that I didn’t learn about pension early enough when I got my job, so I only later adjusted the risk profile. And that I didn’t research investing more before doing it, which made my trading fees quite high. But learning comes with time.

What financial goals are you working towards?

I want my monthly savings plan to reach £29,300, and I want to fill up my stock savings account.

Beyond that, my goal is to ensure I can reduce my working hours or retire earlier if I want to.

Who is your financial role model, and why?

My parents. They taught me to prioritise what you spend money on and that money can go far if you are intentional.

What I Spent in a Week

Day 1 – Monday: £2,047

• Car leasing payment: £292

• Puppy: £1,755

Total: £2,047

Day 2 – Tuesday: £591.80

• Heating etc.: £500

• Mobile subscription: £10.50

• Internet: £35

• Medication: £46.30

Total: £591.80

Day 3 – Wednesday: £34.60

• Toys etc. for puppy: £34.60

Total: £34.60

Day 4 – Thursday: £0

• No spending

Total: £0

Day 5 – Friday: £145.45

• Puppy items: £131.55

• Takeout: £13.90

Total: £145.45

Day 6 – Saturday: £0

• No spending

Total: £0

Day 7 – Sunday: £0

• No spending

Total: £0

Total weekly spend: £2,818.85

Reflections on My Spending

It wasn’t an unusual week, except for the puppy. Overall, my spending habits haven’t changed much since being a student.

The main difference is that I now allow myself to eat out or get takeaway more often, and I include money for hobbies in my budget.