21/2/26

What I Spent This Week as Self-Employed Artist Making £34K

Ever wondered how others really manage their money?

Ever wondered how others really manage their money?

In the A Week in My Wallet series, we share it all, because talking about money shouldn't be off-limits.

Every week, an anonymous member shares a week of their spending: no names, no filters, just honest stories about life's everyday financial choices.

Ready to join the conversation and help make money talk less taboo? Share your own story via our form here.

Monthly Take-Home Pay (after tax): €2,100 (£1,827) budgeted for based on average self-employed income.

Do you share expenses with someone? No

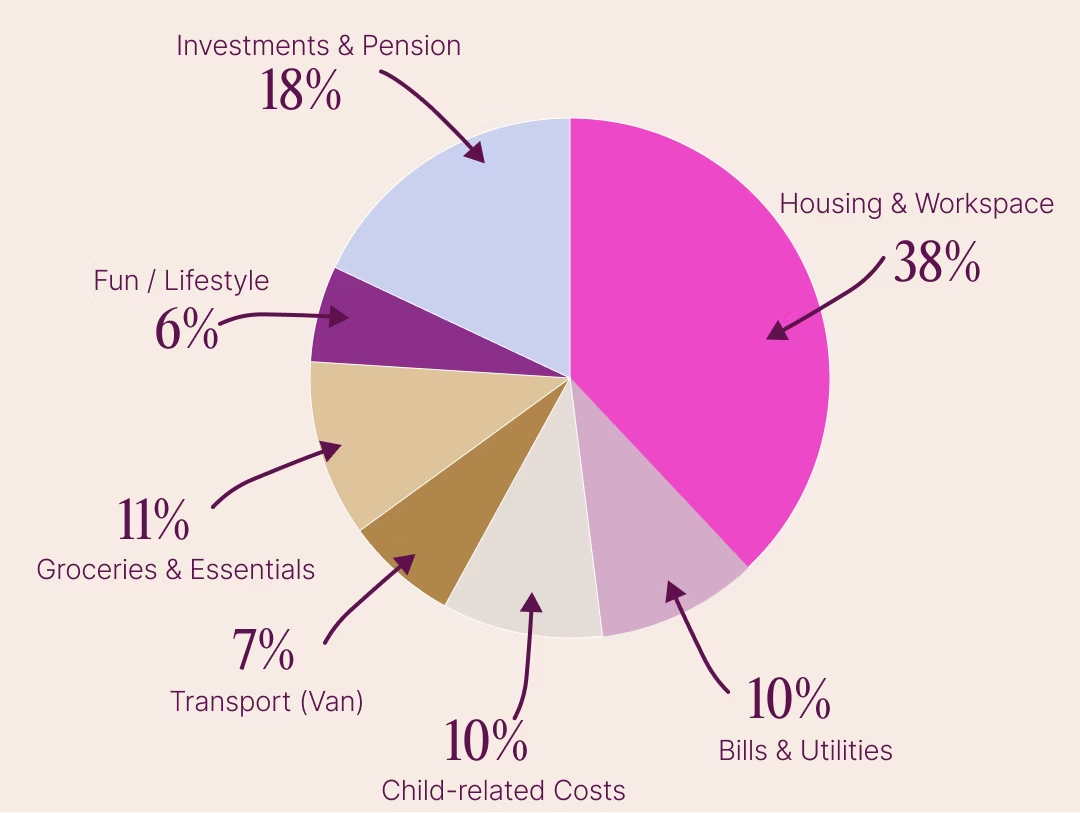

What is your overall monthly budget?

- Rent of my flat, my parking space and my storage unit for work equipment - €800 (£696) a month all together

- Bills - €200 (£174) a month

- Shared account with my ex to cover son’s school meals, trips and material, as well as his extracurricular classes and sometimes for his clothes or meals out the three of us - €200 (£174) a month

- Van (diesel/ tax/ insurance/ maintenance and repairs) - €150 (£131) a month average, it changes monthly

- Groceries (for myself and my son) - €235 (£204) a month

- Fun money (I include here my gym and climbing, as well as things like haircuts, but soon I will start paying into a separate pot for haircuts and cosmetic purchases) - €125 (£109) a month

- Investment contributions - pension €125 (£109)

- Investment fund €150 (£131)

- ETFs and son’s investment account €115 (£100)

I sometimes make purchases of work material and this money is not really accounted for, I usually just try to time it during a month I spent less on the van. I’m freelance and self-employed, so my budget is an estimate based on average income, but there are absolutely months I earn more and months I earn nothing at all.

My self-employed tax and social security payments and accountant fees come to somewhere around - €400 (£348) a month. This money is not included in the budget I have constructed for myself.

Amount left each month after essentials (to spend, save or invest):

0 based on my budget, but my essentials (rent/bills/groceries and son’s expenses) come to €1,500 (£1,305) more or less. The remaining is organised into €150 (£131) investment fund, €125 (£109) pension, €115 (£100) ETFs and son’s investment fund, and €125 (£109) fun money.

Dependents (if any): 1 son

My Relationship with Money

Growing up, did your parents or guardians educate you around money?

Not at all.

What was your first job and why did you get it?

I was 13 and it was as a stablehand, cleaning up after, feeding and caring for horses. I didn’t get much pocket money from my Mum and I wanted more!

Did you worry about money growing up?

As a child I knew we didn’t have much money, my mum was a single parent and there were times we received free school meals, but I didn’t worry about it.

When I was a teenager there was a Government-run initiative to keep kids from low-income backgrounds in school studying their A levels post the obligatory secondary education. It was means- tested and I qualified for the maximum payment which was €34 (£30) a week. It seemed great to me at the time, and I felt very well off!

As a young adult I spent money recklessly and was unwilling to concentrate on things like budgets. Money flew out of my hands as soon as I got it and I started to feel anxious and out of control when it came to money. I took out loans and credit cards and had a very YOLO attitude, which I think I adopted because my mum always took out loans and credit cards. I didn’t want to miss out on anything, and usually did the thing, bought the thing, went on the trip, even if it meant I was paying with borrowed money.

I managed to pay off my debts after I moved in with my ex-partner and began sharing costs. I’ve not been in debt since and the thought really worries me now.

At what age did you become financially responsible for yourself and do you have a financial safety net?

I left my family home at 17 years old and was never able to move back again due to space issues and younger siblings taking my bedroom. I have been financially responsible for myself since then. I don’t have much of a financial safety net, which terrifies me now as I am a single parent, so I’m working hard to budget my money and save and invest absolutely everything I can spare after the essentials to try to build up a safety net and a secure future, for myself and my son.

Do you worry about money now?

Yes, I have nobody to fall back on now. I am a single parent and have to pay for everything by myself and my income is irregular and unstable. I struggle to save because I also like nice things, and being frugal can be depressing, so I’m trying to educate myself as much as I can and take control of the situation. The tools Female Invest provide have helped me so much.

What is your biggest money regret?

Firstly, not educating myself as soon as I left home at 17. Anything financial felt very overwhelming to me and my impulse control was low, I just behaved hedonistically without pausing to think about the consequences. If I had started investing then, I think my life would be very different now.

Secondly, I regret how finances were handled in my long-term relationship. I was with my son’s father for ten years, and during that time we split costs 50/50, even during the nearly 2 years I couldn’t work due to having a baby and losing my job in the pandemic. His attitude was that 50/50 was fair, and I don’t harbour resentment because I know he didn’t fully understand why it wasn’t fair, but I regret not insisting on a different conversation.

On top of this, we did not open a joint account until the last year of our decade together, so until then I was paying him and I never saw the bills. Although I trust the amounts he told me to be true, the dynamic has never sat right with me and I regret not making being open with money an absolute priority. During the relationship I paid half of everything, even when I had no income, which resulted in him being able to save every month whilst I was exhausting my savings in order to contribute to our expenses. I was doing all of the unpaid labour of house work and childcare, whilst he continued to be able to work and earn. I left that relationship without a penny to my name and it was the most awful feeling, I feared homelessness and I feared not being able to care for my son.

What financial goals are you working towards?

I want to buy a house in the countryside. My priority is a roof over my head, and renting makes me feel anxious. The rental market is disproportionately expensive and I could be evicted or any number of things which are out of my control. I’m contributing monthly to an investment fund with a view to using that money in 5-7 years time to get a mortgage or buy a plot of land.

Who is your financial role model (if any), and why?

A friend of my parents is a self-made millionaire. He was born into a low-income family and is a very talented constructor. He found a niche and has made a successful business out of it. I admire anyone who is wealthy because of their own hard work and intelligence.

Reflections on My Spending Habits:

I bought a lot of work tools this week. It makes me feel slightly anxious because for work-related extras like this I use unbudgeted money from my work account and just hope that I am left with enough at the end of the month for my automated self payments and my social security/tax and accountant fees. It’s hard to determine what is a useful investment in my career and what is just an overspend justified by being for work.

What I Spent in a Week

Day 1 – Monday: €434.84 (£378)

€250.45 (£218) - paints and material for a job this week. I will include this cost in my invoice and the client will pay me back when they pay the invoice.

€184.39 (£160) - DIY store. I bought a new tool. Every now and again I invest in a new piece of equipment which will help me at work. Today was this day! I was already in the store buying the paint I needed for work and although this tool will help me on this specific job it’s also a tool I’ve wanted for months and will help me on other future jobs as well. I also bought a few small pieces of wood and accessories to do a carpentry craft activity with my son.

Day 2 – Tuesday: €62.64 (£55)

€49.89 (£43) - Diesel

€1.95 (£2) - pen I impulsively bought for my son in the gas station. It was a snake pen and he loves snakes.

€10.80 (£9) - lunch whilst out on a job.

Day 3 – Wednesday: €0 (£0)

No spend day, I was at home and holding out on a grocery shop.

Day 4 – Thursday: €7 (£6)

I worked from home and made meals from what I already had at home. During their ‘happy hour’ I went to the climbing gym for a reduced price climb. I paid for climbing from my ‘fun money’ pot.

€7 (£6) - climbing gym

Day 5 – Friday: €32 (£28) (€16 (£14) my half)

€32 (£28) - direct debit payment for an after-school club for my son. Taken from a shared account with my ex-partner so the cost is split.

Day 6 – Saturday: €130.86 (£114)

I ran out of fresh food and went to the supermarket

€77.52 (£67) - groceries in Lidl (I will try to make this shop last two weeks, although I will need to top up fresh fruit and veg next week)

€33.48 (£29) - paid on a separate work card in Lidl for a work- related tool

€21.87 (£19) - Bon Preu supermarket. I couldn’t find everything I wanted to buy in Lidl so came here and spent €21.87 (£19) but used €9 (£8) of accumulated funds on a loyalty card.

€6.99 (£6) - henna powder to dye my hair at home. Bought from fun money pot with dedicated virtual card.

Day 7 – Sunday: €0 (£0)

No spend day.

Total Weekly Spend: €667 (£581)